|

|

|

|

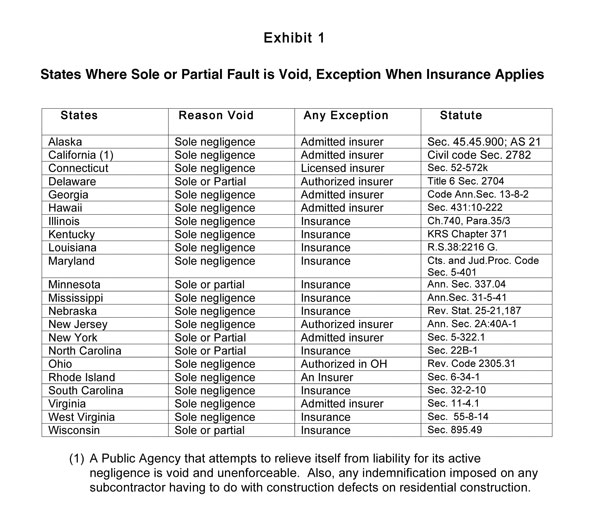

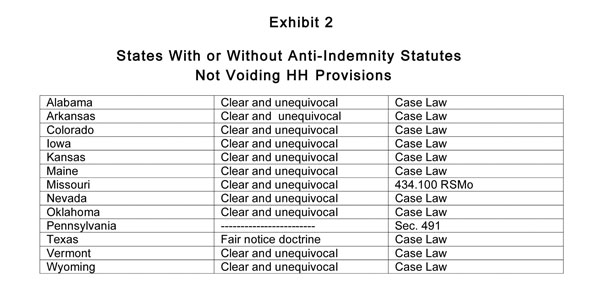

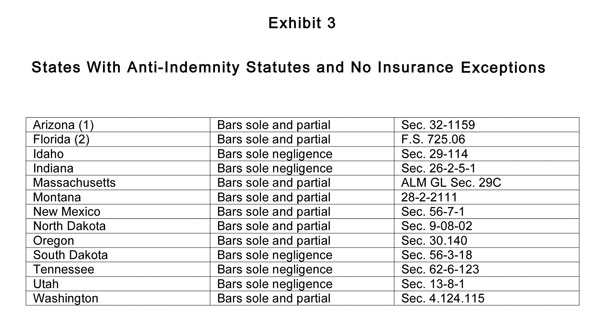

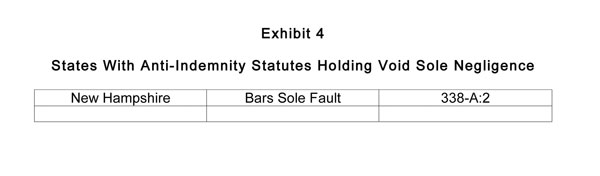

Risk Management Contractual liability undergoes changes Producers will need to study state statutes and individual contract language By Donald S. Malecki, CPCU Until recently, contractual liability coverage under commercial general liability and umbrella/excess liability policies was largely ignored, particularly when a broad additional insured endorsement was available, and one often was. The situation is a little different now, in light of recent changes to narrow the coverage of both standard ISO and independently filed additional insured endorsements of some insurers. Some years ago this column described the choice between contractual liability and additional insured coverage as the “belt or suspenders” concept. In other words, only one of these was necessary: the broader of the two. Currently, however, it can be difficult to determine which of the two alternatives is broader, because endorsements are available to cut back contractual liability coverage, as well as additional insured status. What complicates matters is that if broad contractual liability or broad additional insured coverage or both are prescribed in a contract, and otherwise permitted by law, the coverage provided may fall short of the mark. Taking contractual liability coverage first, the standard CGL policy since 1986 has automatically covered the sole or contributory negligence of the indemnitee (the one who attempts to transfer the sole or partial financial consequences of his or her liability) assumed by the indemnitor (one who assumes such a transfer of risk). All that has been necessary to activate coverage was an indemnitee’s contract requiring such assumption (sole or partial fault) and the absence of any statute holding that assumption void and unenforceable. This broad, automatic coverage, however, was short-lived. In 1988, ISO introduced a contractual liability limitation endorsement, CG 21 39, which has the effect of eliminating paragraph g. of the “insured contract” definition dealing with tort liability assumed. When issued, this endorsement keeps intact contractual liability coverage, but limited solely to what is referred to as L-E-A-S-E agreements; that is, lease agreements, easement or license agreements, agreements required by municipalities (except for work to be performed), railroad sidetrack, and elevator (or escalator) maintenance agreements. Then, in 2004, ISO introduced another endorsement, which has the effect of limiting contractual liability coverage, although it is not as narrow as the preceding endorsement CG 21 39. Referred to as the amendment of “insured contract” definition CG 24 26, it provides coverage for tort liability assumed only in those situations where the indemnitor (the one who agrees to hold the indemnitee harmless) or anyone acting on the indemnitor’s behalf causes the injury or damage in whole or in part. If the indemnitor is not at least one percent at fault, in the situation other than where someone is acting on its behalf, no coverage applies to the indemnitee. The latest additional insured endorsement for owners, lessees or contractors, CG 20 10, introduced in 2004, attempts to align its coverage scope with the coverage provided by the amendment of insured contract definition provided in endorsement CG 24 26. Whether that result will materialize remains to be seen. Where the states stand Producers are likely to hear a lot of dialogue or read articles to the effect that most states have statutes holding void and unenforceable the sole or partial fault of indemnitees. As a result, producers are led to believe that requests for broad coverage are not necessary. Some indemnitors, such as subcontractor groups, would like indemnitees to believe this, but the evidence reveals otherwise. Exhibit 1 shows the 22 states that hold contractual assumptions of sole and/or partial fault to be void, except when some form of insurance applies. (Reference to insurance precludes, in most cases, self-insurance.) What is very important to note, and what may come as a surprise to some, is that five states in this exhibit, Alaska, California, Georgia, Hawaii and Virginia, require that for sole fault assumptions, the insurance must be written with an admitted insurer. Conversely, this means that for partial fault assumptions, the insurance can also be written by a nonadmitted insurer. Exhibit 2 shows the 13 states that do not void hold harmless provisions, so long as the contractual provisions of the indemnitee, in attempting to transfer the financial consequences of its liability to the indemnitor, are “clear and unequivocal” in their intent. The status of these states has come about by statute or case law. Texas, with its fair notice doctrine, is similar in intent to the other states in this exhibit. Exhibit 3 lists the 13 states where both sole and/or partial fault assumptions are considered to be void and unenforceable without exception. If a state voids both sole and partial fault assumptions, this means that the only hold harmless agreements permitted are mutual or reciprocal or “knock-for-knock.” An example of these agreements is where the indemnitor agrees to hold harmless and indemnify the indemnitee for liability caused by the indemnitor, and the indemnitee likewise agrees to protect the indemnitor for whatever liability is generated by the indemnitee. Note that these agreements do not involve the assumption of tort liability. Unless these agreements involve a lease, easement, agreement with a municipality, railroad sidetrack or elevator (escalator) maintenance agreement, they are not considered to be an “insured contract,” as defined by the CGL policy! Exhibit 4 consists of one state and its peculiar way of dealing with contractual assumptions. By exception, partial fault assumptions are permitted whether covered by admitted or nonadmitted insurers or handled through self-insurance. What it all means It is not unusual today to find indemnitees, despite their bargaining power, compromising their contractual risk transfers by accepting “knock-for-knock” contracts. As explained, this means that neither party (indemnitee nor indemnitor) is accepting the other party’s tort liability for bodily injury or property damage. In a situation like this, it would not matter if the indemnitor’s CGL policy were endorsed with the contractual liability limitation endorsement CG 21 39, which removes tort liability assumed coverage, because none is being assumed anyway. Conversely, this means that a CGL policy unendorsed with a contractual limitation, or the amendment of insured contract definition CG 24 26, would be of no significance, since neither would be necessary. This same conclusion applies to the 13 states listed in Exhibit 3. Where both sole and partial fault assumptions are void and unenforceable, without exception, contractual liability insurance is unnecessary. What is left is liability that the insured would have in the absence of a contract or agreement, and that is covered by exception to the contractual liability exclusion. What may be of significance are the 22 states comprising Exhibit 1, which permit sole and/or partial risk assumptions, with certain insurance exceptions, and the 12 states listed in Exhibit 2, which permit sole and/or partial fault when the contractual assumptions are “clear and unequivocal” in intent. Let’s assume, for example, that an indemnitee imposes a contractual assumption involving sole fault in any one of these 34 states and the indemnitor’s CGL policy is unendorsed with a contractual limitation endorsement. The indemnitor’s CGL policy should apply, if the indemnitee is sued for its sole fault tort liability. If, however, the CGL policy is endorsed with either one of the two contractual liability limitation endorsements, coverage may be insufficient, leaving the indemnitor exposed to a suit for breach of contract for failing to procure the coverage promised. Additional insured status Were it not for the recent changes affecting additional insured endorsements, it would not likely matter what the status of contractual agreements is by state. However, such is not the case today. As a result, it could turn out that both the contractual liability and additional insured coverages are insufficient where sole or partial fault is being assumed in one of the 34 states in Exhibits 1 and 2. Also important to note is that the 13 states in Exhibit 3, which bar sole and/or partial fault assumptions, also bar additional insured endorsements providing sole and/or partial fault coverage—something that insurers may have overlooked in the past. Now insurers will need: (1) to be careful about issuing additional insured endorsements where they are not permitted, and (2) to be more reasonable in their underwriting process than simply issuing contractual liability limitation endorsements carte blanche without considering the situation. Caveat for producers Today, there are far too many pitfalls confronting insurance buyers, particularly those whose exposures involve contractual liability or additional insured status or both. Producers no longer have the luxury of simply requesting that a broad additional insured endorsement be issued to cover the insured’s sole or partial tort liability. The situation today requires someone to read the contract and determine what is being transferred or assumed, whether it is permitted by law, and whether the policy will cover that exposure. Some producers, particularly those who do niche marketing to contractors or developers, may undertake this added role of reading contracts and consulting with their insureds (the persons or entities directly retaining the producer’s services) about the coverage being provided and whether it is adequate for the situation. In the majority of cases, however, the time has come for producers to employ good risk management sense by transferring the obligation of reading contracts and determining their validity with the insured’s attorney. Only after this legal task is completed can the producer attempt to see if the proper coverage can be provided. If coverage cannot be provided, it would behoove the producer to notify the client. Author’s note: The comments and observations here are not intended to be legal opinions nor the practice of law. No action or inaction should be taken on the basis of these comments or observations without reviewing these statutes or proposed legislation or by consulting appropriate legal counsel. * The author |

|

|||||||||||||||||||||

| ||||||||||||||||||||||