|

|

|

|

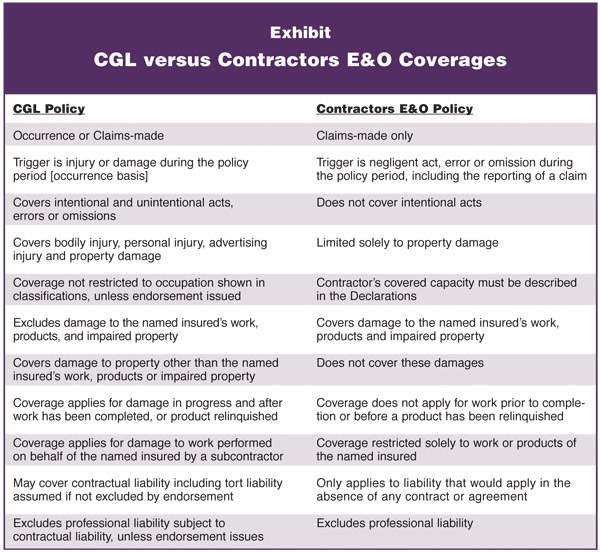

Risk Management Contractors errors and omissions Contractors E&O provides protection beyond a CGL policy By Donald S. Malecki, CPCU A producer wanting to offer liability coverages for contractors beyond what little is now being provided through the commercial general liability policy (CGL) may wish to consider coverage, however limited, for business risks. Among the specific business risks are: damage to the insured’s work, products, and impaired property. With great frequency, courts rule against coverage for contractors because of damage to the work they have performed, whether or not it is properly labeled as the contractor’s “work” or “product.” Producers might be somewhat skeptical about any insurer willing to provide this coverage, since business risks are supposed to be assumed by those who create them. While producers are not too far wrong, some policies have been sold covering these risks—but with very narrow coverage, as one should expect. Because insurers offering this specialized coverage do not commonly stay in the market very long, producers also should consider the longevity of the insurer offering this coverage. A standard line insurer might be a better choice, other things being equal, than an insurer specializing in these coverages. Producers need to understand that it is not contractors professional liability insurance that is necessary here but, instead, contractors errors and omissions insurance. This might appear to be nothing but a subtle difference. In actuality, however, there is a lot of confusion between the terms “professional” and “errors and omissions” liability. In fact, the very first rule to keep in mind is not to rely on policy coverage titles. So, while it is the contractors errors and omissions policy that has been known to provide coverage for certain business risks, the coverage may turn out to be available under an entirely different coverage name. Reviewing the provisions, therefore, is crucial. A discussion of contractors professional liability coverage is for another day. Briefly, however, this insurance is necessary for contractors with professional liability exposures, such as those involved in construction management and design-build projects. Policy references to “professional’ and “errors and omissions” may suggest a coverage different from general liability insurance. While this is true, it would be a mistake to assume that these policies close all gaps if they are written together. In fact, both the contractors professional, and contractors errors and omissions polices generally limit coverage to negligent acts, errors or omissions—a limitation not found in general liability policies. Narrow coverage characteristics It is a good idea when reviewing a contractors errors and omissions policy to determine its coverage characteristics for producers have a good understanding of the commercial general liability policy. The reason is that producers will be able to single out what the CGL policy excludes, what potential problem areas may exist, and whether the contractors errors and omissions policy is appropriate for the contractor in question. The accompanying exhibit points out differences between a CGL policy and a contractors errors and omissions policy intended to cover a contractor’s business risks. Generally, the contractors errors and omission policy is written on a claims-made basis. Although it is likely that the policy will require that the negligent act, error or omission take place during the policy period, some policies make an exception for a negligent act, error or omission that takes place prior to the policy’s inception. The usual conditions precedent are that no other insurance is available and the insured did not know or could not have reasonably foreseen that such negligent act, error or omission might be the basis of a claim or suit. What can be troubling about these special contractors policies is that the coverage is contingent on the named insured’s negligent act, error or omission and the property damage must arise from the contractor’s covered capacity or role as described in the policy declarations. With the standard of care limited to a negligent act, the insurer desiring to deny coverage can simply maintain that the named insured’s decision to perform work that turns out to be faulty was intentional rather than unintentional. With various coverages limited to negligent acts, court decisions are on the increase. Some, in fact, have been discussed in earlier issues of this column. One contractors errors and omissions policy excludes damages arising out of any intentional decision by the insured to substitute a material or product or deviate from a process or procedure that was specified on blueprints, work orders, contracts or engineering specifications unless there has been written authorization. One could understand that such a deviation should be excluded. But what happens when the intentional decision turns out to be an honest mistake? Can the insurer still have grounds to deny coverage? The obvious answer will likely depend on how serious the claim is. The fact that the contractor’s role or business capacity has to be described in the policy probably is an insurer safeguard to prevent extension of coverage beyond any other work that the contractor undertakes that has not been underwritten. Thus, unlike in the CGL policy, coverage would not extend to new activities that arise during the policy period. Of course, some insurers can simply endorse the CGL policy to apply the same type of restriction by limiting coverage to the classifications as shown in the policy. Coverage under these policies is limited to property damage, as defined in the policy. This means that the contractor has to rely on its CGL policy for (1) bodily injury, personal and advertising injury coverages, (2) property damage to property other than the named insured’s work, product or impaired property, and (3) liability assumed under contract, except for liability that the insured would have in the absence of a contract or agreement. The foregoing exclusions are the common ones found in contractors errors and omissions policies. A review of these policies will likely produce several more that clarify what specifically is intended with regard to these narrow policies. Some of the exclusions found in these special policies also will correspond to those of the CGL policy, such as environmental impairment, asbestos, and property damage to property owned, rented or leased to the insured. Unique criteria What makes this coverage especially unique is the fact that coverage is limited to the negligent acts, errors or omissions of the named insured which, if an entity, would include its partners, members, executive officers, directors, and employees. These policies do not cover work performed on behalf of the named insured by a subcontractor. This requirement that coverage not apply to damages caused by the subcontractors enables the underwriter to better underwrite the risk, and it is likely to reduce the frequency of claims—if underwriters are selective about whom they accept for this coverage. It is unfortunate but nonetheless true in many cases that defective claims can arise simply because some general contractors use the criterion of the lowest bidder instead of retaining the services of quality subcontractors. This sometimes results in problems—something an underwriter of the contractors errors and omissions policy does not have to worry about. The unique criterion of this policy is that the property damage must occur after the work (impaired or otherwise) has been completed, or the product has been relinquished. This may be a problem because it is not always clear when damage first occurs. A case in point is Advantage Homebuilding, LLC v. Maryland Casualty Co., 470 F.3d 1003 (U.S. Ct. App. 10th Cir. 2006). Three homeowners brought a suit against the general contractor who constructed their houses. Some windows were scratched when the subcontractor dropped mortar on them. The damage to the windows was discovered after work had been completed and owners had occupied the houses. The insurer maintained that since the windows were damaged when the work was in progress, the exception to exclusion (L) of the CGL policy, for damage to work performed on behalf of the named insured (general contractor) by a subcontractor did not apply. Instead, damage was excluded because of the CGL policy’s exclusions (j)(5) and (6), which apply while operations are in progress. Briefly, exclusion (j)(5) excludes property damage to that particular part of real property on which the named insured or any of its contractors or subcontractors working on the named insured’s behalf are performing operations, if the property damage arises out of those operations. Exclusion (j)(6) excludes that particular part of any property that has to be restored, repaired or replaced because the named insured’s work was incorrectly performed on it. With the slightest proof that any damage happened prior to completion of the work, insurers most assuredly will challenge a claim that may meet all other criteria. In fact, this may be fairly easy to prove, unless the event giving rise to damage consists of an inherent defect not easily discernable until after damage occurs. With the contractors errors and omissions policy available solely on an claims-made basis, producers need to determine the requirements necessary to determine when a claim is considered to be reported. Determining the availability and price of an extended reporting period also is important. Deductibles also are commonly required. Conclusion Given that contractors errors and omissions coverage is intended to cover certain business risks that commonly are excluded by liability policies, coverage not only is going to be narrow in scope but also will be subject to a variety of conditions where contractors have to work on the straight and narrow, if a claim is to be paid. The overall price of coverage is likely to be the major obstacle. Producers desiring to make this coverage available to their contractor insureds need to practice good risk management skills in order to reduce any chances of misunderstanding. On that score, producers should point out (preferably in writing) that this insurance:

The author |

|

|||||||||||

| ||||||||||||