|

Here is a possible loss scenario:

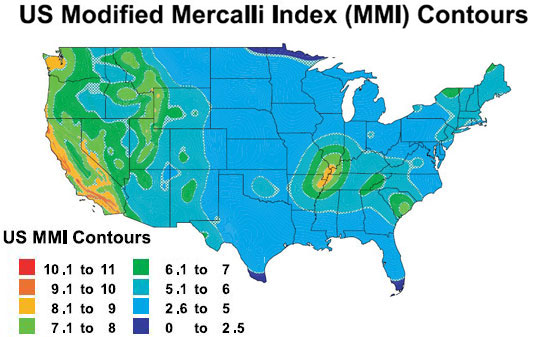

The New Madrid fault shifts and vibrations are felt in Missouri, Tennessee, Kentucky, and into Indiana and Ohio. Millie, in southern Indiana, is jolted awake at the sound of her beautiful porcelains crashing to the floor. When she inspects her home shortly after dawn, she discovers that the top of her chimney is gone, the fallen bricks from it having crashed through her solarium windows.

She is even more dismayed when she drives to the hotel complex she manages and discovers that the earth movement shook the building's foundation, causing the elevator shaft for the exterior glass elevator to shift slightly, resulting in the elevator no longer being usable. |

|

|

Our experts listed Endurance, Westchester, ICW, Arrowhead, RLI, Aspen, RSUI, Alterra, Northshore, Axis, Arch, Chubb, Commonwealth, Markel, WesternRe, London, Bermuda, American Empire, Chartis, ACE, Lloyd's, and Beazley as companies actively writing earthquake coverage in the United States. This list could expand considerably if the standard markets that write earthquake as part of all risk coverage were added.

Rob Kish, executive vice president; property brokerage at Crump Insurance Services, Inc., says, "The majority of E&S markets write on nonadmitted paper. There are a few exceptions, like ICW, that write on admitted paper. The factor is E&S placement versus standard market placement. Standard markets write on admitted paper."

"The carrier advises if the risk is eligible for admitted paper for the locations being submitted," explains Tina A. LaRocca, executive vice president of AmWINS Group, Inc. "After thoroughly marketing the risk, we then present all options to our retailers and it is ultimately up to the insured to decide. With commercial earthquake policies, only a handful of carriers are able to offer admitted paper in California."

According to Andy Roe, vice president–commercial lines underwriting at Arlington/Roe & Co., Inc., "The main factor impacting admitted versus nonadmitted status is the state where the risk is located." He then added the following regarding rates, "They vary greatly between non-quake/less quake-prone areas versus quake-prone areas. Non-quake-prone areas have a high percentage of $500 minimum premiums."

Mr. Kish explains, "Pricing is also driven by the type of buildings, geographic area, and the model carriers use to track their exposure in a particular quake zone or its proximity to a fault. The pricing for a location in San Francisco would normally be much higher than in San Diego. In non-quake-prone areas, it's a minimum charge to include the coverage in an all risk program."

Availability and pricing go together. "If you are in an earthquake-prone area, the rates will be significantly higher, and the market's ability to put up capacity will differ greatly," says Ms. LaRocca. "For example, a carrier may be able to offer only a $5 million limit on a location in Los Angeles that is worth $20 million in building values at a rate of .30/$100. However, put that same type of building in Arizona and the same carrier may be able to do the full $20 million for .05/$100."

Click here for the complete article … |

|