|

| |

Companies/Brokers/MGAs

Do you have a new product or enhancement?

Click here to submit your information

—OR—

call 1-800-428-4384 to speak to

Eric Hall Vice President / National Sales Director - Advertising. |

|

| |

| INSURANCE MARKETPLACE SOLUTIONS |

|

| |

|

|

Mini wraps

A major coverage problem in the residential construction marketplace is being solved on the west coast with a general liability only wrap-up sometimes called a mini wrap. Since the problem is becoming more national in scope, will the mini wrap also become the national solution? This edition of The Insurance Marketplace® Cybercast reviews the residential construction marketplace, some problems with the mini wrap and specialty insurance markets ready to offer solutions. |

| |

|

|

| |

| The Residential Construction Marketplace |

| |

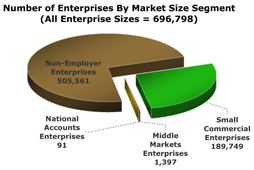

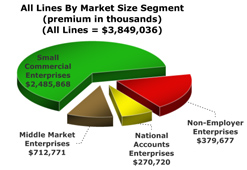

The residential construction marketplace consists of nearly 700,000 enterprises producing close to $4 billion dollars in property/casualty premium. Most of the premium comes from non-employer and small commercial enterprises. Over $2.75 billion premium is developed by the more than 690,000 businesses. The fewer than 1500 national and middle market enterprises account for a little less than one billion in premium. These numbers are very conservative because they do not include any premium for residential subcontractors and remodelers.

For more information:

MarketStance Web site: www.marketstance.com

E-mail: info@marketstance.com |

| |

|

| |

| The Wind is Coming from the West |

| |

It has been more than 10 years since construction defect losses created an insurance crisis in California. Condominium and residential home developers – particularly those with homeowners associations – began to feel the insurance market tighten, premiums rise and limits drop. The crunch started with general contractors and quickly worked down to the subcontractors and sub’s subcontractors. General contractors demanded coverage from their sub contractors that the subcontractors could not obtain.

The insurance industry does not allow problems to go unsolved for long. The solution for the residential construction industry was a unique type of residential general liability-only wrap-up coverage called a mini wrap. Most wrap-ups are primarily cost saving financial products that lead with Workers Compensation coverage. They are characterized by large projects, high premiums and limits and intense loss prevention and safety measures. By comparison, the mini wrap is a coverage driven product. It includes only general liability coverages, has fairly low limits, applies to small to medium-size projects and incorporates standard loss prevention efforts. While many brokers enthuse about the advantages and financial freedom of the large project wrap-ups, many mini wrap agents and brokers accept the mini wrap as the only solution available saying “It’s not perfect but isn’t it better to have $1,000,000/$2,000,000/$2,000,000 limits with some coverage than no coverage at all?” |

| |

|

| |

| A Sub Trapped In A Wrap |

| |

|

To better understand the coverage concerns, consider this example:

Presley is a plumber who works on new construction, repairs and remodels. He has been with the same agent and company for years with no losses. All of his recent new construction jobs have required his joining the insurance wrap-up on the project or not get the work. His insurance company requires CG 21 54 be attached to his policy, eliminating coverage for all work done on wrap-up projects. He doesn’t protest since he has coverage under the wrap.

Presley receives a call from Heavenly Homes Association to complete some warranty repair work. His employee, Quentin, makes the service call. Quentin trips over his shoelaces and falls on the condominium unit owner Millie, causing her to fall down her steps. She sues Quentin and Presley for her injuries. Presley reports the claim to his agent who informs him there is no coverage due to the wrap-up exclusion. Presley then reports the claim to the agent handling the wrap-up. That agent informs him that there is no coverage because the project is complete. Presley thought he was well protected but must now to handle the case on his own.

It turns out that there are more problems at Heavenly Homes. Presley is named in a lawsuit against the developer for plumbing-related construction defects. Since Presley knows his insurance company will not provide coverage, he contacts the wrap-up agent. The agent informs him that the Heavenly Homes wrap-up will not respond because the $2,000,000 aggregate is exhausted by payments made to settle other cases. The insurance company won’t even defend him! |

| |

|

| |

Brad Tennant, President of Tennant Special Risk, explains how the marketplace responded to the California residential market crisis. “The GL only, smaller, residential wrap-up started in California and other states which had developed a reputation as ‘construction defect’ states. Traditional residential contracting writers pulled out of those construction defect states as Plaintiff Attorneys were able to apply class-action provisos to the states’ construction defect laws. As a result, plaintiffs were able to name every contractor that worked on a project to their suit and apply what some have termed ‘green mail’ to elicit settlements from contractors”.

The wrap-up was a logical response. The market was limited at the beginning. “Five or six years ago, Clarendon and Aspen were about the only two markets for GL-only, residential wrap-ups”, according to Marc Adler, senior vice president with Colemont Insurance Brokers in Arizona. “Today more than a dozen national carriers plus a handful of regional carriers are responding. This is opening up the possibilities and solving some of the problems that have emerged.”

Click here for the complete article … |

| WHO IS WRITING GL RESIDENTIAL WRAP-UPS? |

|

|

| |

Richard B Usher, Principal Managing Member of Arizona retail broker Hill & Usher travels the country doing workshops for trade contractors contemplating entering into wrap-up agreements and he cautions the contractors to “deal with a professional agent to assist in getting involved in a wrap-up. The professional agent will assist the contractor to assess the quality of risk and risk sharing elements of the wrap-up”.

Do you need help in finding an expert who is actively working in this market place? Insurance Marketplace has talked to the following markets who are interested in writing Residential Wrap-ups:

BROKERS

MANAGING GENERAL AGENTS

INSURANCE COMPANIES |

| |

| |

|

|

|

|

|

|

| |

| |

This message was sent by The Rough Notes Company, Inc.,

11690 Technology Drive, Carmel, Indiana, 46032

1-800-428-4384

|