|

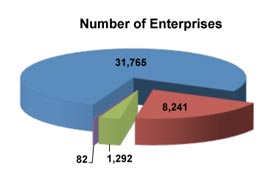

Movies and books glamorize the world of private detectives and security operations, representing them as bastions of individualism. According to the market information, the myths may actually be true. Over 31,000 enterprises have no employees. However, the media doesn't tell the entire story. Nearly 1,200 of these operations are considered middle market enterprises and they pay over $100 million in premiums each year.

For more information:

MarketStance website: www.marketstance.com

Email: info@marketstance.com |

|

Here is one possible claim scenario.

Mitchell Security has a contract with the Julius Hotel to provide security. The contract specifies that the guards are to patrol the sidewalks, parking lots and hallways at set times. Freda’s room is on an upper floor at the rear of the hotel nestled in the woods. When she walks out onto the balcony, the door behind her closes and automatically locks. When her cries for help over a period of four hours go unanswered, she decides to take action and attempts to climb down. She falls, breaking her arm and leg, but is found by a guest occupying a ground floor room. Freda sues the Julius Hotel and Mitchell Security for her injuries. Mitchell Security defends itself by showing that there was no sidewalk in the area around her room. It also points out that, since her balcony was not visible from either the parking lot or the hallway, it was impossible for their guards to be aware of her situation. |

What is the primary exposure for a security or investigative agency? According to Karen Izzo, president of Izzo Insurance Services, Inc., one often overlooked is, “The result of contracts intentionally drafted to transfer liability to the security company when the security company has no control over the situation giving rise to the claim.” Torrence W. Brownyard, CPCU, president of Brownyard Group states, “Because security guard claims involve complicated indemnity and additional insureds, it’s important that the program manager or the insured offer a dedicated and knowledgeable claims facility.”

David Toombs, vice president commercial underwriting of Arlington/Roe, Inc., points out some types of security situations that might be difficult to place, including heavy crime areas with low income housing, airport security, any type of power plant, armored cars, military bases, bounty hunters, repossession operations, bodyguards for celebrities, municipal buildings in high profile cities or situations, certain types of political rallies and certain types of concerts. Mr. T. Brownyard adds that some international exposures, such as security contractors doing work in the Middle East, are also hard to insure.

What coverages should each of these agencies consider as primary? Peter Costanza, president of Costanza Insurance Services says, “In addition to workers compensation, a security firm should have a commercial general liability (CGL) policy that includes errors and omissions, personal injury, full care, custody and control coverage, and assault and battery coverage.” According to Bruce W. Brownyard, president of Brownyard Programs Ltd., the errors or omissions/professional is a particular concern. He believes that “particularly for a guard company, the financial loss from an errors or omission loss is most significant, yet many of the carriers really don’t go there.”

Mr. T. Brownyard adds fidelity coverage and, "depending on the specifics of the firm, umbrella liability, auto, property and EPLI coverages.” Mr. B. Brownyard agrees with the need for fidelity coverage but warns that the coverage must be reviewed carefully. The security guard company needs a third-party rider so that coverage extends to the client’s property and coverage should not include a conviction clause since most guard thefts don’t end up in convictions, because of plea bargains, etc.

Click here for the complete article … |