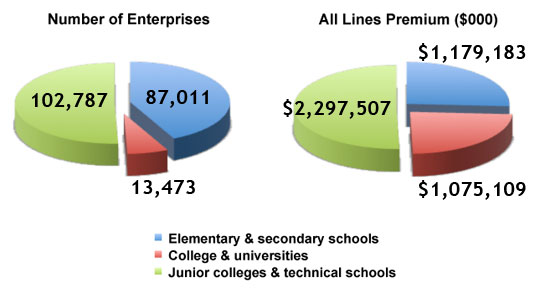

The marketplace for educational institutions is quite varied. Some insurance companies and brokers that provide the coverage have very broad appetites while others are more limited.

“We specialize in private, K-12, community colleges, small- to mid-size four-year colleges, small- to mid-size universities, and various types of vocational/technical schools,” explains Shirl Hedges, underwriting manager at Philadelphia Insurance.

Tony Armor, commercial underwriter/business development at Roush Insurance Services, Inc., says, ”We can place coverage for all types of educational institutions. However, we most often receive submissions for vocational/technical schools such as construction, welding, and apprentice training.” He states that these types of risks are usually written on nonadmitted paper.

WRM America is in the market for most types of schools. Its president, Steven E. Sims, says, “WRM America provides a comprehensive program of coverages to public and private K-12 schools, public and private colleges and universities, and vocational/technical schools.”

Connie R. Reynolds, vice president, school programs at Glatfelter Public Practice, explains that it has a slightly different approach. “We write private and public K-12, junior colleges, and community colleges, but we don’t write universities. We write vocational/technical schools, but not driver training schools or certain others. We can also write nursing school programs and other two-year programs.”

School exposures include property, liability, automobile, EPLI, and workers compensation. According to Ms. Hedges, two unique and important exposures are failure to educate and violent events.

Mr. Sims points to the broad nature of the exposure. “Complicating traditional risks is the fact that schools are often used by outside parties and members of the general public for activities such as religious services, recreational sports leagues, elections, and other community events."

“From a liability standpoint, the most common exposure is sexual/physical abuse and injury to students or athletes," according to Mr. Armor. "With schools placing a great deal of emphasis on athletics and academics, many students spend almost as much time at school with training, practices, tutoring and/or research as they do at home. As a result, there is greater potential for both bodily and personal injury for athletes and other students who may find themselves in situations that could compromise their safety.”

Ms. Reynolds adds, “There have been several high profile cases of bullying recently. Incidents of bullying create serious issues for schools because they can involve physical injury, emotional distress and civil rights violations. Schools are also at risk because of the personal data of their employees, students and parents that they maintain electronically. All of which could be subject to theft by a hacker.”

The exposures can vary significantly by risk. One school may have a large property schedule while another has bus transportation issues because of its remote location or special needs students. The recent economic downturn also brings the potential for layoffs that could lead to EPLI claims and workers compensation issues.

The types of claims also vary by type of school. According to Ms. Hedges, “For academic schools and vocational schools, the greatest issues involve property. About 90% of my book's large losses come from property exposures like wind, hail, fire, and sprinkler failures. The past year’s winter storms added significant property losses that involved weight of snow and ice.”

Mr. Armor agrees with Ms. Hedges and adds, “Many educational institutions do not have enough manpower to maintain multi-facility campuses. Regular maintenance issues are often ignored and later cause problems that could otherwise have been prevented.” He suggests that educational institutions look for carriers with specialized loss prevention and claims services that may help them mitigate property losses.

Slips and falls are the most frequent claims, according to Mr. Sims. These are mostly on school playgrounds, sidewalks, and at athletic facilities. He adds, “The most severe claims involve sexual misconduct and hazing incidents.” WRM America offers seminars and training sessions on these exposures as an important tool in addressing and managing these losses.

Most markets that work with educational institutions provide all lines of coverage. According to Ms. Hedges, these include property, inland marine, general liability, sexual abuse, educators' liability, directors and officers liability, EPLI and umbrella liability. Mr. Armor recommends that the general liability include injury to athletes. He also recommends student accident and health insurance and international coverage if students and faculty travel abroad.

Mr. Sims says, “The most common coverage gap we see for educational institutions is for law enforcement. We often see law enforcement with sub-limits or sharing limits with other coverages, which is insufficient for a school.” Adds Gail Pierce, senior commercial underwriter at Roush: “Employed security guards may be excluded. Coverage can often be added by endorsement, but sometimes a separate policy is required.”

Property coverages and limits are a concern, according to Ms. Hedges. “Schools should make sure they have appropriate property coverage with adequate building limits and business income limits. They should have either crisis management or violent event response coverage, which can address extra expenses that may occur when the institution must be shut down such as security services, public relations and counseling services. She also believes that outsourcing of services should be reviewed carefully. School policies often respond only to claims that involve employees. The use of self-employed consultants could be a problem, especially if they are unable to purchase coverage as individuals.

Ms. Reynolds sees many coverage enhancements being offered because of the competitive market. She says, “Ordinance and law, pollution liability, and expanded property may be available. On the general liability side, enhancements may include a broad definition of named insured that possibly picks up the school's parent-teacher organization and professional liability for school nurses. On auto, Glatfelter offers replacement cost on buses that are 10 years old or less.”

Our experts all agree that there is a vibrant and active marketplace for educational institutions. Pricing, although generally competitive, varies with the nature of the institution. Some segments of the market appear to have been stable for a few years, while others saw significant drops in 2009 and are now leveling off. As schools have been forced to cut back on activities, employees, and building projects, premiums have also declined because the exposures are reduced.

The educational institutions market is broad and offers many opportunities, and it changes as the educational system changes. There is increasing diversity in types of schools, activities provided, and teaching approaches. Schools are expected to provide both physical protection during the school day as well as psychological damage protection from bullying and cyber attacks on students and faculty that might occur at any time. As these expectations grow, so does the institution’s need for a knowledgeable insurance agent, insurance company and risk manager. |