INSURANCE MARKETPLACE SOLUTIONS

Insurance Agents Errors and Omissions

This month, it's all about you.

Insurance agents are not computers, order takers or golfing/fishing/shopping buddies. They are highly trained professionals who are responsible for working with a client in developing a comprehensive plan to protect vital assets.

There are many types of insurance products. There are many professional designations. There are many specialties and specialists. However, in the end all agents have one thing in common. When a loss occurs, the client is depending on them to have placed the promised coverage.

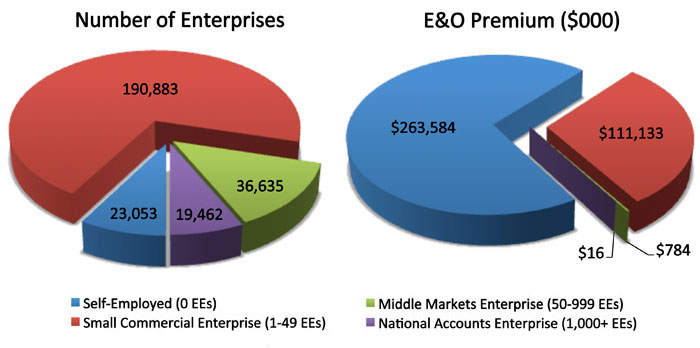

GROWTH POTENTIAL

The vast majority of insurance agents are small commercial enterprises. There are a number of self-employed agents, but most agents work with a larger enterprise and obtain their E&O coverage and many other services through that other enterprise. Over 70% of the E&O premium is paid by the small commercial enterprise.

For more information:

MarketStance website: www.marketstance.com

Email: info@marketstance.com

STATING THE OBVIOUS

The insurance agent is the conduit linking the insurance buyer to the insurance carrier. The agent is expected to be able to communicate in both the language of the client and the language of the carrier. Unfortunately, claims can happen because something is lost in translation.

The best way to avoid the communication problem is documentation. A checklist of recommended coverages can lead to discussions about coverages a client may not have considered in the past. The checklist also allows the client to clearly indicate when coverage is desired and when it is not desired.

A written procedure describing how your agency interacts with clients will help your staff be the professionals your clients deserve and also will prevent misunderstandings.

THE HEART OF THE MATTER

Here is a possible scenario:

Karina has written Paul's insurance for many years. She has his homeowners, auto, boat and umbrella coverages placed with one of her best carriers. When Paul married Sharon, he invited Karina to the wedding. Karina was the first to know that Paul had bought Sharon a car because she added it to his auto policy.

The marriage encountered some turbulence, and Sharon took the car and moved out.

Paul stopped by Karina's agency one day to talk. He explained the separation and his hope of reconciliation. Karina sympathized with Paul and wished him the best but never discussed or reviewed the insurance implications. Unfortunately, about four months after the separation, Sharon was in a car accident. She was badly injured, and the occupants of the car she struck were also injured.

Paul called Karina, who immediately notified the insurance carrier. The carrier did a thorough investigation and denied coverage because the policy listed only Paul as the named insured. Sharon had been away from the residence for over 90 days, so his auto policy no longer covered her.

Sharon and Paul did reconcile, and together they sued Karina because she had never recommended that Sharon be added to the auto policy as a named insured. They also recast the conversation in Karina's office as an insurance consultation, not a just a friendly chat, and they said that at that point Karina should have told Paul about the 90 days' residency requirement. Karina has no documentation to dispute their assertions.

Karina's insurance agents errors and omissions policy may be paying for all of the damages.

THE MARKETPLACE RESPONDS

The market for insurance agents errors and omissions coverage is robust. The Independent Insurance Agents & Brokers of America and the Professional Insurance Agents offer coverage through their state associations. Other insurance associations sponsor programs for their membership. However, these are not the only options.

Glenn W. Clark, CPCU, owner and president of Rockwood Programs, Inc., explains their unique approach to this coverage. “The market for agent E&O is always in flux. The programs offered by the large national agent associations tend to change carriers to keep members’ premiums from increasing too much. At Rockwood, that’s not our market. We target niches that aren’t served by association programs, like newly licensed agents, crop insurance agents, and agency clusters.”

The road less taken is also the approach of Innovative Risk Solutions. John Watt, ARM, vice president, says, “We arrange coverage for retail agencies, specialty wholesale and surplus lines brokers, MGAs and underwriting managers, and insurance consultants who operate on a fee for service basis rather than earning commissions on the sale of insurance products.”

Linda Blechman, assistant vice president-insurance agents’ professional liability at Lee & Mason Financial Services, Inc., explains that they take a slightly different approach. “Our policy is available to licensed property/casualty and life/health agents and brokers and to wholesalers, general agents, managing general agents, and program administrators. We can extend coverage to insurance consulting, premium financing, claims adjusting, loss control, and risk management services. Coverage also is available for the sale of variable life insurance, variable annuities, and mutual funds.”

There are both admitted and nonadmitted markets writing this coverage with some being placed in London

Mr. Clark explains that the coverage offered through Rockwood varies based on the services provided by the customer. They have four different types of coverage so that they can be as responsive as possible. As an example, “We have a program for newly licensed P/C agents with one to three years’ experience who offer only standard lines of business and generate less than $150,000 in gross commission revenue annually; the deductible is $5,000, and limits are $500,000/$500,000 or $1 million/$1 million. Agents insured under this program are eligible for the standard program after they have three years’ experience.”

The exposures vary based on the type of agent. Ms. Blechman says, “For retailers, whether property/casualty or life/health, failure to document coverage discussions with insureds is a major cause of frequency, and it also can cause severity. Frequency also is an issue for small retail agencies that are generalists who must master the details of many different kinds of policies and sell coverage to a wide range of classes. Severity can be a problem for retailers who place property coverage in coastal areas that are subject to hurricanes and flooding.”

Mr. Watt adds, “On the retail side, we see frequency when the agent doesn’t clearly explain coverages to the client or fails to offer coverages; when binding authority is violated, and when internal procedures are not followed. Failure to communicate clearly to the insured what is and is not covered also can contribute to severity when the insured sustains a large loss that the policy doesn’t cover and alleges that the agent either failed to offer coverage or told the insured that coverage was in place when it was not. Without proper documentation, these situations often turn into a ‘he said, she said’ dispute. We recommend that all of our agencies have a written procedures manual and have a system in place for formal documentation of all conversations and communications with their insureds.”

“Frequency is much less of an issue for large wholesalers, MGAs, and program managers that offer only one specialized product to a market whose exposures and needs they understand very well,” according to Ms. Blechman. “That said, some specialty classes, like long-haul trucking, are very high maintenance and require the MGA or wholesaler to make frequent coverage changes because of driver turnover and changes in routes or cargo. Here frequency is an issue for agencies that don’t have procedures in place to ensure that change requests are documented and that changes are made on a timely basis.”

Mr. Clark adds, “Across the spectrum of agents we insure, the greatest frequency comes from (a) failure to procure coverage that the insured either asked for or should have been asked to buy and (b) lack of proper documentation. The insured has a loss, reports it to the agent, and then finds out that it isn’t covered. If you lack proper documentation, it’s very difficult to prove that you actually did what you say you did, or that you did what you always do in the same situation. Those cases usually go in favor of the client and against the agent. “

What are the key underwriting criteria? Mr. Watt says, “A major red flag is lack of written procedures. Related to that is the lack of an effective automated system that creates a suspense for each activity in a client’s file, triggers a follow-up, and clears the item when the activity has been completed. The lack of such a system is an accident waiting to happen.”

One severe loss is less daunting to our experts than a frequency of smaller claims. Mr. Clark explains, “For agents who have a claim history, we have three remedies: (1) don’t insure them, (2) increase the premium to take account of the increased exposure, or (3) risk modification by excluding certain kinds of activities or using a high deductible so the insured participates more in his own losses.”

The actual application submitted to the underwriter can be an indicator of the how the agency itself operates, according to Ms. Blechman, “As an underwriter, I sometimes see applications that are so sloppy that I can hardly read them. If an agent’s E&O application looks like this, what does that say about how they run their office and handle their documentation? If I have a clean, legible app and an app with sloppy handwriting and coffee stains, which one do you think I’m going to work on first?”

The insurance agents errors and omission marketplace has substantial capacity but is firming. The agencies that use best practices of established written procedures and effective documentation will not only provide the most professional service for their clients, they can also expect to receive the most comprehensive coverage and attractive pricing.

WHO WRITES INSURANCE AGENTS ERRORS AND OMISSIONS COVERAGE?

MANAGING GENERAL AGENTS

Contributing to this article:

Innovative Risk Solutions, Inc.

P.O. Box 530210

DeBary, FL 32753

Contact: John Watt, ARM, Vice President

Email: jwatt@irs-incorporated.com

Phone: (954) 931-4795

Website: www.irs-incorporated.com

Rockwood Programs, Inc.

4001 Miller Rd.

Wilmington, DE 19802-1999

Contact: Glenn W. Clark, CPCU, Owner and President

Email: glenn.clark@rockwoodinsurance.com

Phone: (302) 765-6000

Toll Free: (800) 558-8808

Fax: (302) 764-5477

Website: www.rockwoodinsurance.com

PROGRAM ADMINISTRATOR

Contributing to this article:

Lee & Mason Financial Services, Inc.

195 Farmington Ave., Ste. 301

Farmington, CT 06032

Contact: Linda Blechman, Assistant Vice President-Insurance Agents Professional Liability

Email: lindab@leeandmason.com

Phone: (877) 562-4311, ext. 404

Fax: (860) 677-1227

Website: www.leeandmason.com

|