INSURANCE MARKETPLACE SOLUTIONS

Banks

We need them!!!

Large, medium, and small banks are vital to almost every aspect of our personal and business lives. Every community knows that a thriving bank enhances its economic security.

The insurance industry plays an important role in keeping banks healthy. They have many exposures that can and should be insured. However, like many insureds, they need help to effectively identify hazards and manage risk appropriately.

Are you ready to help?

GROWTH POTENTIAL

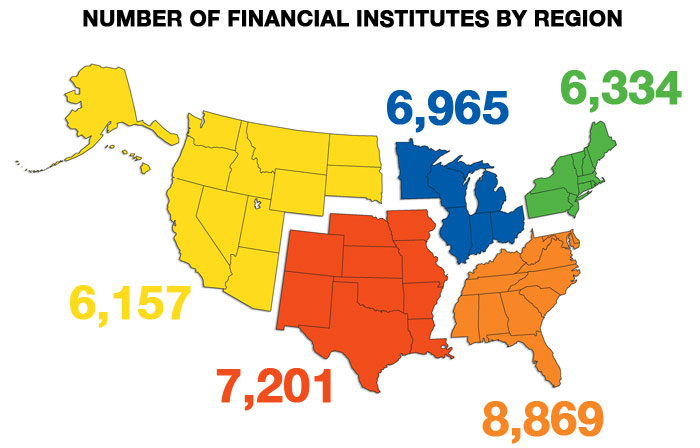

This graph includes many types of financial institutions. The largest percentage is banks with 61%, credit unions at 30%, and savings and loans with 9% of the total. Over 60% of these institutions are considered small commercial enterprises with between one and 49 employees. There are 365 national banks and 5,379 middle market banks but over 29,000 smaller banks. The anticipated growth rate for all banks is 4.4%, but the smallest banks are expected to grow almost 8% over the next two years.

For more information:

MarketStance website: www.marketstance.com

Email: info@marketstance.com

STATING THE OBVIOUS

Banks are commercial enterprises and need most standard types of commercial insurance. However, because of the role they play in the economy, they have some unique exposures that can be covered only by products specifically designed for them.

THE HEART OF THE MATTER

Here is a possible scenario:

James and Karen purchase their first home. They obtain a mortgage through Good News Bank. They meet at the bank to sign the papers and take possession of the property. Everything goes well, but as they leave, Karen slips on the wet floor in the lobby. She breaks her arm and makes a claim against Good News that its insurance carrier settles.

Karen’s injury causes her to miss too many days at work and she loses her job. She cannot find another job, and soon she and James have problems paying their bills. Their homeowners insurance is one casualty. Good News Bank force places coverage on their behalf and adds its cost to their monthly mortgage payment. A fire occurs when James leaves a pot on the stove too long, and the forced place policy responds to the loss.

The fire loss adds even more stress to Karen and James’s situation. They are underwater on the house, cannot handle their bills, and decide to declare bankruptcy and walk away from the property.

Good News Bank forecloses on the house and takes it over. It cancels the force placed coverage and adds the vacant property to its owned real estate commercial insurance coverage. The bank’s coverage responds when a neighbor child is injured on the property.

Karen is furious! She applied for a job and had a good chance of getting it until personal information Good News Bank had in its computer system was somehow passed on to her potential employer. She sues the bank for breach of privacy. Good News Bank’s cyber liability policy provides a vigorous defense.

THE MARKETPLACE RESPONDS

Most standard insurance carriers can provide the traditional property and casualty coverages that banks need: commercial property, general liability, commercial auto, equipment breakdown, computer-related inland marine coverages, accounts receivable, valuable papers, and workers compensation.

Anthony Davis, president of Anthony R. Davis Agency, lists some of the specialty coverages that banks may need:

- Mortgage Impairment Insurance (Mortgage Errors & Omissions)

- Mortgage Servicing Force Placed Fire and Flood Coverage

- Bankers REO Coverage

- Flood Determination Services

- Bankers Blanket Bond

- Bankers D&O Liability Coverage - Including Entity Coverage

- Bankers Specialized Property and Liability Coverage

- Employment Practices Liability

- Voluntary Optional Mortgage Coverage - Life, A&H, AD&D

- Credit-Related Coverages - Fixed and Revolving

- Blanket Fire (First and Second Mortgages)

- Environmental Impairment Liability Coverage

- Lender Liability

Some of these coverages are optional, but many (such as the bankers blanket bond) are required by government regulations.

This Cybercast focuses on two bank-specific coverages needed to round out an account.

Oliver Brew, vice president of Miscellaneous Professional Liability and Technology E&O at Liberty International Underwriters, provides information on cyber liability. Lisa Cooper, John Watt and Greg Shimkus at Innovative Risk Solutions provide information on forced place and bank-owned property coverages.

Read the complete article here

WHO WRITES BANKS?

MANAGING GENERAL AGENTS

INSURANCE COMPANY

|