|

| |

Companies/Brokers/MGAs

Do you have a new product or enhancement?

Click here to submit your information

—OR—

call 1-800-428-4384 to speak to

Eric Hall Vice President / National Sales Director - Advertising. |

|

| |

| INSURANCE MARKETPLACE SOLUTIONS |

|

| |

|

|

Adjusters Errors and Omissions

Independent adjusters represent the insurance company, while public adjusters represent the claimant. Since all are trying to objectively determine the value of a claim, they have quite a bit in common, including a significant errors and omissions exposure. They are charged to fairly represent their clients by adjusting losses based on the facts of the insurance policy and the loss that occurs. The problem is determining what is fair. Independent adjusters and public adjusters are not hired for the normal. They are hired when a problem exists, such as major weather catastrophe or when specific expertise is demanded. This heightened interest in a particular loss or loss situation has the potential to result in litigation with respect to the adjuster’s activities.

|

| |

|

|

| |

| The Adjusters Marketplace |

| |

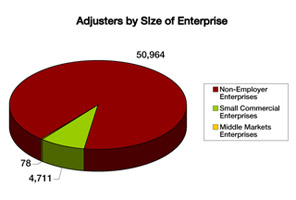

The adjuster’s marketplace is primarily made up of individual adjusters. Nearly 51,000 businesses have no other employees, while only about 5,000 are small commercial businesses and less than 100 qualify as middle market accounts. The total number of these enterprises grew by 2.7% in the past two years and anticipated growth is 2.3% for the next two years. The fastest growing segment in continues to be the sole proprietorship with no employees.

For more information:

MarketStance Web site: www.marketstance.com

E-mail: info@marketstance.com |

| |

|

| |

Policyholders pay insurance companies premiums in exchange for the promise that they will pay policyholder claims for losses, according to the terms and conditions of the policy. In most cases, when a claim is presented, an insurance company employee works directly with the policyholder to settle the loss. If the claim is not settled to the policyholder's satisfaction, the insurance company can be sued. This sequence of events can change dramatically when an independent adjuster or public adjuster is involved.

While these different types of adjusters are independent contractors, the one thing they have in common is that each works on a fee basis. Public adjusters receive their fees from the policyholder, while the independent adjuster receives its fees from the insurance company. Unfortunately, these fees can result in conflicts of interest. The public adjuster may be accused of exaggeration, enhancement or fraud in order to inflate the fee, while the independent adjuster may be accused of ignoring legitimate damage, settling liability claims too quickly or undervaluing the cost of repairs in order to please the insurer. Any of these activities can result in an errors or omissions claim against the claims adjuster. |

| |

|

| |

|

To better understand the coverage concerns, consider this 1997 Texas court case:

William C. Dear & Associates (Dear) was hired to investigate the mysterious death of jockey Dan Beckon. The client, Barbara Russo, was unhappy with how the investigation was progressing and subsequently sued the investigator. The Scottsdale Insurance Company provided the professional coverage for Dear and hired Hammerman & Gainer (H&G) as independent adjusters to investigate the case. When Scottsdale settled the suit with Russo, Dear sued Scottsdale, its law firm and H&G. The argument against H&G was that it breached its good faith duty to Dear and to Scottsdale because of pressure from the law firm. The court ruled that H&G had no duty to Dear, since the relationship was between the carrier and the adjuster. Since there was no duty owed, there was no duty to breach.

The good news for H&G was that it was not liable. The bad news was that it incurred considerable defense expense.

(William C. Dear and William C. Dear & Associates, Inc. V Scottsdale Insurance Company, Paul B. Van Ness, Johnson & Sylvan, P. C. and Hammerman & Gainer, Inc.) |

| |

|

| |

Adjusters errors and omissions coverage is available to independent adjusters and public adjusters. It protects their interests when a client or a claimant sues them for neglect or breach of duty. One of the major problems is that the coverage may appear to be an unnecessary expense.

Since independent adjusters work with insurance companies, they may believe they are protected by the company they represent. However, Lee Helms, underwriting vice president of Claim Professionals Liability Insurance Company (RRG) (CPLIC), suggests that, “All adjuster firms, including one person firms, should have their own E&O coverage and not rely on coverage extended by larger firms for whom they are working as independent contractors.” While some coverage may be provided by the client insurance company, there is no protection for the adjuster firm if the company brings a suit. In addition, since the representation by the insurer will be on behalf of the insurer, it will be biased in favor of the carrier. The adjuster has little or no input as the carrier negotiates.

Jeanie Cardon, at Hall & Company (MGU for Travelers Insurance Adjusters E&O Program) provides some additional reasons why adjusters should purchase their own coverage. “Local adjusters are often named in a suit so that a loss will stay in the local jurisdiction and not go to a federal court, which may not be as favorable to the claimant. If the adjuster is ultimately released from the suit it is not without claims handling expense and time, which with E&O coverage is handled by the carrier. Without coverage, the adjuster is taking time away from her or his adjusting business to address the claim, not to mention the out of pocket expense.”

Considering all the attention independent adjusters received following hurricanes Katrina and Rita, as well as after the 2006 spring storms in the midwest, is the marketplace still willing to write adjusters?

Click here for the complete article … |

| |

| WHO IS WRITING ADJUSTERS? |

|

|

| |

WHOLESALE BROKERS

MANAGING GENERAL AGENTS

INSURANCE COMPANIES |

| |

| |

|

|

|

|

|

|

| |

| |

This message was sent by The Rough Notes Company, Inc.,

11690 Technology Drive, Carmel, Indiana, 46032

1-800-428-4384

|