INSURANCE MARKETPLACE SOLUTIONS

Pet-related Services

Who will be waiting for you when you walk through your door tonight? For many of us, the most excited family member will be a pet. While our pets provide companionship, it has been determined that they also reduce our stress levels and increase our ability to tolerate pain. They can provide security and a sense of peace during chaotic situations. Is it any wonder that the pet-related services industry continues to show positive growth even during the current economic downturn?

Pet-related services discussed in this Cybercast are pet walking, pet sitting, kennels, pet day care facilities, trainers, and groomers. Although some veterinarians and veterinary clinics have pet boarding facilities, they will not be addressed here, nor will animal shelters and pet rescue operations.

GROWTH POTENTIAL

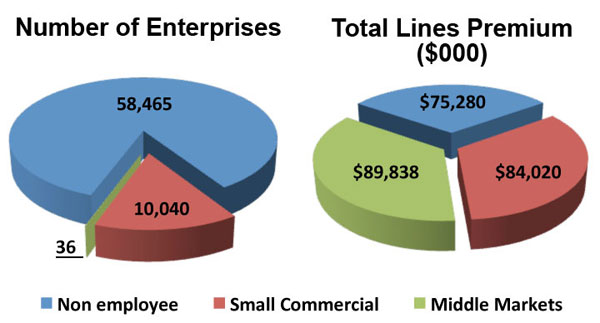

The pet-related services industry is growing. The information in this graph is based on 2010 data. MarketStance estimates that this industry will experience a 7% growth rate over the next two years. The growth in the non-employee class is estimated to be almost 8%. The fact that so many providers of pet-related services are individuals keeps this industry from gaining any significant national traction. Pet stores have tried to add some of these services, but the revenue from services is declining, not increasing. This suggests that pet stores are reducing theses services instead of increasing them. It appears that the majority of pet-related services will continue to be provided by individuals rather than becoming part of larger operations.

STATING THE OBVIOUS

A pet is an important part of its owner's life. When the pet must be left with a caregiver or service provider, the owner is concerned that the pet will be cared for properly. The owner also wants assurance that the pet will not damage the owner's property or the property of others, or cause injury to others. The expectation is that the caregiver entrusted with the pet's care will provide the same loving and responsible care as the pet's owner.

THE HEART OF THE MATTER

Here is a possible scenario:

Mandy is pet sitting the Martin family's three dogs and two cats while the family is on a two-week vacation. Her contract requires that she visit the home no fewer than three times during each day. On one of those visits, she must take the dogs on at least a one-mile walk. She must ensure that all of the pets have food and water in the amounts specified and also administer medication to the older cat.

On her morning visit, Mandy leashes the three dogs for their walk. Everything goes well until Charlie (the Great Dane) becomes overly excited and darts toward a woman walking past him. He is overjoyed to see her, jumps against her, and knocks her to the ground. Her outfit is ruined and she has difficulty standing. Mandy apologizes profusely as she helps her up.

Mandy receives a notice from the woman's lawyer three weeks later stating that she is expected to pay for the damage to the woman's clothing and the medical expenses she incurred.

Mandy submits this information to her homeowners insurance carrier. However, the insurer informs her that she is not covered for any of the damages because she was conducting a business and her policy does not have a business endorsement.

THE MARKETPLACE RESPONDS

Standard markets can provide coverage for pet service operations. The coverage can be written on businessowners policies or commercial package policies. It can also be written by attaching a business endorsement to a homeowners policy. This approach can satisfy many of the coverage concerns. However, there are unique exposures that standard policies may not cover. This Cybercast explores these exposures with specialists who are familiar with issues in the pet-related services industry.

Potential customers must be identified. David Springer, President, Programs Division at NIP Group, Inc., explains, "Most dog walkers and pet sitters are emerging businesses operated by individuals, and many of these people are not aware of the need to secure insurance." These individuals typically love animals. They may care for the animal at the animal's home or at the sitter's home. More and more, these micro-businesses are becoming aware of the need for insurance.

Mr. Springer explains, "Someone who goes into a customer's home to provide pet care services faces many of the same exposures as individuals and businesses that do housecleaning and provide other in-home services. A frequent cause of claims is when the pet sitter or dog walker loses keys. If a key can't be found, the lock may have to be replaced. The pet sitter may cause property damage or be accused of stealing items that belong to the pet's owner."

Additional exposures arise because the animal is a living creature. Mr. Springer says, "Because of weather, illness, car trouble, or other factors, the pet sitter or dog walker may not get to the customer's house in a timely manner, and the pet may be deprived of food and water or medicine. In other cases, it may injure itself, become ill, or cause damage to property."

Individuals who perform dog walking services also have liability exposures because they are responsible for controlling the animal. If a dog being walked bites or injures a third party in some other way, the dog walker could be found negligent and responsible for the damages.

Some pet service providers know they need insurance coverage but may not be aware of the need for specialized coverage. "Professional liability coverage is needed but may be overlooked", says Kelly Spencer, Program Manager, PetPro™. (PetPro is an all-lines insurance program developed by NIP Group for a wide variety of pet care providers. It is written on admitted paper.)

Read the complete article here

WHO WRITES PET-RELATED SERVICES?

PROGRAM ADMINISTRATORS

|