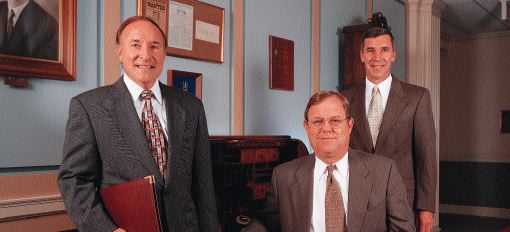

Harleysville executives gather at the roll-top desk which belonged to the company's founder. From left are: Spence Roman, executive vice president of field operations and subsidiaries; Walt Bateman, chairman, president and chief executive officer; and Bob Jaso, senior vice president of marketing and business development.

* Deliver superior insurance products and related services to our customers

* Achieve consistent, profitable growth to enhance stakeholder value

* Provide growth opportunities in a learning environment for those who contribute to our success

A quiet town nestled deep in placid Pennsylvania Dutch country probably seems to be an unlikely venue for the headquarters of a major all-lines insurance organization with subsidiaries operating in 31 states. The fact is, however, that since 1917, Harleysville, Pennsylvania, population 10,735, has been headquarters for the Harleysville Insurance Companies, a group of regional insurers located throughout the eastern, midwestern and southern United States.

What today is known as Harleysville Insurance originated in 1915 as an association formed by the town's leading citizens to spread the risk of automobile theft. Organized by businessman Alvin Alderfer, who was concerned by the theft of several Ford sedans in the area, the association was modeled on the horse theft societies used by local farmers for many years to share the costs of replacing members' stolen horses. Each of the association's 102 members paid a small monthly fee into a fund that paid the cost of recovering or replacing any member's stolen car.

In 1917 the association was granted state charters as the Mutual Auto Theft Insurance Company and the Mutual Auto Fire Insurance Company (two entities were formed because state law at the time prohibited one company from selling both automobile and fire coverage). Fast forward more than 60 years to 1979, when Harleysville Group, Inc., was formed to manage a growing family of subsidiaries, chief among which were Harleysville Mutual Insurance Company and Harleysville Life Insurance Company. Publicly traded since 1986, Harleysville Insurance today operates a network of regional insurers in 31 eastern, midwestern and southern states (see sidebar below), offering a full line of property/casualty and life insurance, as well as surety bonds, risk management, and asset management services. With almost 2,700 employees and more than 3,000 independent agents, and 1997 consolidated assets of $2.4 billion, Harleysville today ranks 52nd on A.M. Best's list of 1,200 leading property/casualty insurance companies and groups.

Old-fashioned values for a new age

It's a long road from 1917, when more people owned horses than cars, to today's ultra-high-tech world of complex risks and big numbers. Over those 80-plus years, Harleysville has grown at a steady, measured pace and, by sticking with its core values, has built a national network of insurers whose success owes much to a strong commitment to regional underwriting. Harleysville is clearly an insurer that lives up to its mission statement (see box on page 38), which encompasses all parties to the insurance transaction. In this article we'll talk with several of the company's top executives to find out how Harleysville views itself, its policyholders, and its agents, and the course it's charting for the year 2000 and beyond.

"We make it a point to adhere to the discipline of underwriting...

"We make it a point to adhere to the discipline of underwriting...

--Walt Bateman, chairman,

president and chief executive officer

For many publicly held insurers in today's intensely competitive market, the focus is on the bottom line, sometimes at the expense of sound underwriting. That's definitely not the case at Harleysville, says Chairman, President and Chief Executive Officer Walter Bateman. "In all our news releases about earnings, we make it a point that we adhere to the discipline of underwriting," he declares. "It's what we do for a living, so we want to stick to it and not get caught up in the market conditions of the moment."

Each of the insurers Harleysville operates retains its own identity, has its own management team, and--perhaps most important--underwrites at the local level, using its knowledge and experience in its own market to build a profitable book of business. "Underwriting is strongly influenced by regional and local conditions," Bateman observes. "A property risk of a certain value might be a good risk in one area but a bad risk in another. That's why we underwrite close to the marketplace." What's more, he adds, "We're growing but at the same time, we want to remain local. Our customers don't see us as a monolithic bureaucracy; they feel close to us."

The best of both worlds

"Other companies operate networks of local carriers," says Spencer Roman, senior vice president of field operations and subsidiaries, "but we're different. Rather than having all functions conducted at the local level, we take a 'best of both worlds' approach. When we bring a company into the fold, it continues to operate under its own name and logo and to be responsible for its own underwriting, marketing, and claims. At the home office we handle core functions that can be performed more efficiently at a centralized location: information systems, human resources, accounting. We maintain a regional focus where we need it and consolidate other operations at the home office." This strategy also allows Harleysville to spread its exposure to weather patterns, political environments, and regulatory risks over a broader area.

"We recognize that our network approach involves multiple infrastructures," Bateman observes. "We've been able to offset those costs by achieving better underwriting results in catastrophe-free years."

Shifting gears

As was noted earlier, Harleysville Insurance writes a full line of property, casualty and life products for both individuals and businesses. Until the mid-1970s, the majority of the group's business was in personal lines. As the result of a strategic shift, consolidated commercial lines premiums now account for some 61% of the companies' annual volume. Initially Harleysville focused on writing small and medium-sized accounts, offering a wide array of coverages for a broad range of businesses. "For a long time we've taken a generalist approach to the market, because it was very appropriate for our agency base," Walt Bateman says. "Today many companies are being very specific about what they will and won't write, but a lot of independent agents, especially those in small towns and cities, don't want to be specialists. For that reason, it still makes sense for us to offer a diverse portfolio of products."

Still considering itself a commercial lines generalist, Harleysville is creating more customized programs for agents.

Still considering itself a commercial lines generalist, Harleysville is creating more customized programs for agents.

--Spence Roman, above, states, "We've been increasing our niche marketing for several years."

Although Harleysville still considers itself a commercial lines generalist, more recently it's been placing increasing emphasis on creating customized programs in areas where it sees strong profit potential. Examples are contractors, garages and service stations, restaurants, golf courses, physicians, dentists, lawyers, and wholesalers. "We're making a strong effort to offer 'hooks' to our agents," Bateman says. "We want to create new sales opportunities for agents and show them that we're broadening our risk appetite. For instance, the old Harleysville would have shied away from risks like nonstandard auto; the new Harleysville is committed to offering specialty programs in areas where appropriate risk analysis and pricing can generate strong profit potential."

Bob Jaso, above, notes that Harleysville offers a range of services to strengthen the agent-company relationship.

Bob Jaso, above, notes that Harleysville offers a range of services to strengthen the agent-company relationship.

Also convinced of the merits of this focused approach is Robert Jaso, senior vice president of marketing and business development. "Our target marketing effort gives us a good way to compete and do so profitably," he comments. Historically, he notes, Harleysville has tended to pursue mainstream commercial accounts. "Over the last 18 months, we've begun to pursue more middle-market business," he says. "An example is our Millennium line of products, which is targeted toward medium to large commercial accounts." Adds Spence Roman: "The products we've developed over the last three or four years have generated $40 million to $50 million in volume. We've been increasing our niche marketing for several years."

Strong in workers comp and surety

Harleysville's largest commercial line is workers compensation. Several factors contribute to the insurer's success in controlling loss costs in this volatile line: implementation of managed care programs, strict fraud control measures, and direct reporting of claims. Harleysville also participates in workers compensation reform efforts in every state in which it conducts business and plays a leadership role in the workers compensation and medical issues committees of its national trade association.

Harleysville also offers a complete line of surety bonds. Both performance and payment bonds are available for a wide range of contractor specialties; the insurer also writes bid, supply, and other miscellaneous contract bonds. Non-contract bonds offered include public official, license and permit, court and probate, miscellaneous, and program. A dedicated unit pursues surety business as a complement to policyholders' existing commercial lines coverage.

Getting personal

Harleysville offers a full range of personal lines programs, including auto, homeowners, dwelling fire, personal excess and pleasure craft. Pricing is territorially driven on the basis of profit potential. As with commercial lines, the insurer has a broad appetite for personal lines risks, writing family accounts over a wide demographic area. Harleysville has strengthened its competitive position and ability to retain these family accounts through a concept termed generational continuity. This approach involves insuring drivers with appropriate products that keep pace with their changing circumstances from the time they reach driving age through their elderly years. In addition, Harleysville has targeted some specific customer segments within personal lines, such as nonstandard drivers, work site groups, high-valued homes and in-home businesses.

Adding "life" to sales

In the life sales arena, Harleysville is committed to an approach that complements the group's property/casualty-based agency force, believing that to be the most effective strategy in the life insurance market. This approach includes an orientation toward:

* Competitive group insurance products designed to meet the needs of Harleysville's commercial clients from both a benefit and price perspective. Product line strengths track Harleysville's commercial strongholds.

* Life products that are tailor-made for property/casualty sales. A prime example of this niche approach is a mortgage disability income policy designed specifically for the company's homeowners market.

* Lead generation programs that encourage cross-selling among product lines, helping agents realize the full sales potential for each client.

* Quality products that perform up to the standards policyholders expect from Harleysville. For example, the company's Elite Life III universal life product has placed in the top 10 in A.M. Best's annual survey of UL performance throughout the marketplace.

* A commitment to exploring new avenues agencies will need to compete on the life side as the market changes. The decision to introduce a variable annuity product in the near future is an example of the group's interest in expanding its portfolio to meet changing demands.

* Continued emphasis on field service to agencies to keep them apprised of important changes in the way they market life products.

* Ongoing high-quality customer service to assist and retain existing policyholders.

A complete line of life and health insurance products for both individuals and businesses is available through Harleysville Life Insurance Company. Products offered include basic life insurance, college funding, and mortgage protection for individuals and families, and key employee coverage, simplified pension plans, and debt protection for businesses.

Throughout its 80-plus-year history, Harleysville has remained fully committed to the independent agency system. Its agent longevity figures tell the story of enduring relationships with many producers: of Harleysville's more than 3,000 agents, 67% have represented the company for more than 10 years; and 25% of the agency force has been affiliated with the insurer for more than 25 years. "We aspire to be the first, second, or third leading writer in each of our agencies," Bob Jaso says, noting, "We're currently #1, #2, or #3 in 70% of our agents' offices." A striking feature of the agency-company relationship, he adds, is that Harleysville imposes no minimum volume requirement. "We've found smaller agencies to be quite profitable," he says. "We love it when a company sets an arbitrary volume threshold. We pick up a lot of great agents that way. Some of our agents write only $200,000 with us, but when you put it all together, they are a wonderful source of business for our company."

Walt Bateman agrees. "We're not into the 'You're too small to represent us' mode," he declares. "If an agency has a future, we want to grow with it--size isn't the primary criterion." What are some of the criteria agents must satisfy to form an alliance with Harleysville? "An agency should have strong financials, a good track record with its companies, and satisfactory loss ratios," Spence Roman says. "It should have an efficient operation that's well automated, and it should have in place a solid business plan, proactive marketing strategies and a sound perpetuation plan. Finally, an agency should have the same appetite for risk that we do."

How does Harleysville view its relationships with producers? "Our focus on regionality means we have tighter relationships with agents compared with larger companies," Walt Bateman responds. "We want to work closely with our agents and have a mutual understanding of each other's needs; we want our agents to be co-planners with us."

Adds Roman: "We hear a lot of gloom and doom stories about the future of independent agents. However we're convinced there will continue to be a large segment of customers who will buy through independent agents because they need professional advice and counsel. Our strategy is to identify those customers and provide our agents the products and marketing tools they need to penetrate this market."

Menu of agent services

Harleysville offers its agents a wide range of services designed to foster the mutual commitment it considers essential for sound agent-company relationships. Among those mentioned by Bob Jaso are:

* In-house training and education

* Flexible payment options for agents and clients (direct bill or agency bill)

* Compensation levels that exceed market levels, based on an agency's performance with Harleysville

* Communication vehicles: regional and national Agency Communication Councils, local and regional sales meetings, regional and national newsletters

* Toll-free claims line, available 24 hours a day, seven days a week

* Fast turnaround on quotes, plus online rating

* Lead generation via an agency locator feature on the company's Web site

* Sophisticated loss control and risk management services

* Rewards and incentives program for top agents (Honors Program), plus extra services (for example, co-op advertising and automation support) for agents who satisfy additional criteria (Honors 5 Star)

* Agency Stock Purchase Program--opportunity for best agents to purchase Harleysville Group stock at a discount

* Additional incentives--travel program for profitable production, CSR programs for personal lines, vacation programs for production of select targeted lines (for example, nonstandard auto)

* Agency Partnership Program--offers certain agents greater financial rewards and security in return for increased volume

* Other services--field automation support, access to local branch office underwriting capabilities, development of managed care programs, and access to top management

Sticking to the basics

With today's stormy sea of price slashing and bottom-line management, it's clear that at least one insurer is calmly steering a course toward long-term growth and profitability, simply by adhering to its mission and to its decades-old philosophy of sound underwriting combined with strong, enduring agency-company relationships. Commitment, discipline, dedication--old-fashioned values for the thoroughly modern--and eminently successful--insurer known as Harleysville. *

Harleysville Mutual Insurance Co.

Great Oaks Insurance Co.

Harleysville Asset Management L.P.

Harleysville-Atlantic Insurance Co.

Harleysville-Garden State Insurance Co.

Harleysville Insurance Company of New Jersey

Harleysville Life Insurance Co.

Huron Insurance Co.

Insurance Management Resources L.P.

Lake States Insurance Co.

Mainland Insurance Co.

Mid-America Insurance Co.

Minnesota Fire & Casualty Co.

New York Casualty Insurance Co.

Pennland Insurance Co.

Worcester Mutual Insurance Co.

©COPYRIGHT: The Rough Notes Magazine, 1998