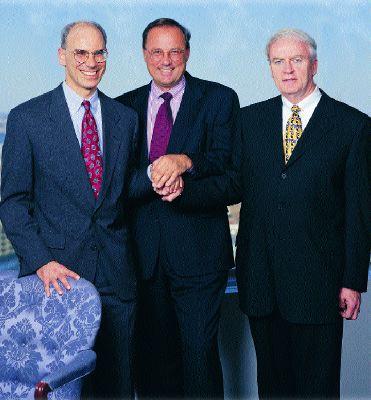

The executive team of the newly merged CGU includes senior vice presidents (left to right) David J. Firstenberg, commercial lines; Richard S. Banas, insurance operations; and Jack Doyle, specialty lines.

When two business entities merge, observers usually wonder which one will come out on top. Understandably, we tend to regard the idea of a true "marriage of equals" with some measure of cynicism.

In the case of CGU, created less than a year ago by the merger of Commercial Union and General Accident, the

"C-word" definitely isn't cynicism. Far more appropriate, in fact, are terms such as cooperation and commitment. In this article we'll talk with top CGU executives to find out why this merger took place, how the combined entity is structured, and what it has to offer its nationwide field force of more than 7,000 independent agents.

"A New 300-Year-Old Company"

Since the merger of Commercial Union and General Accident in June 1998, that's the way the combined organization has been describing itself in communications with the public, investors, policyholders, and agents. Boston-based Commercial Union traces its roots back more than 300 years through its UK parent, Commercial Union plc, with U.S. operations established more than 125 years ago. General Accident, whose Philadelphia-based U.S. operation dates back to 1899, was a subsidiary of General Accident plc, founded in 1885 in Perth, Scotland.

The combined entity, CGU, is owned by CGU plc and has headquarters in Boston. With premium volume of over $4 billion, CGU ranks as the 16th largest property/casualty insurer in the United States. Licensed in all 50 states, CGU employs 7,500 persons and operates through a network of 13 regional offices, 44 branch offices, and some 7,100 independent agents. The CGU Insurance Companies have an A+ pooled rating from A.M. Best.

Merging two major insurance carriers, especially ones as long established as Commercial Union and General Accident, is unquestionably a daunting task. From the start, however, the executives of the combined entity committed themselves to making the transition as smooth, as expeditious, and as beneficial as possible for policyholders, employees, and agents. Plans call for the consolidation to be completed by the end of this year, according to Richard Banas, CGU's senior vice president for technical insurance operations, and thus far things are right on schedule. Banas has executive responsibility for commercial and personal lines underwriting, claims, reinsurance, and strategic planning.

Why did Commercial Union and General Accident merge? "From a U.S. perspective, it took place because our respective parent companies in the United Kingdom merged," Banas explains. "In that sense, it was an 'arranged marriage'--and a great one. In the next one to two years we believe we can accomplish what it would have taken each company 10 years to accomplish on its own." Further, he notes, the combination caused no dilution of the capital base of either company. "It's a true merger, and it's creating a stronger, more competitive company than either of us could have been individually."

"An integrated local team is in place to service the agent's needs, and we do everything we can at the home office to support the local team's partnership with its agents."

"An integrated local team is in place to service the agent's needs, and we do everything we can at the home office to support the local team's partnership with its agents."

--David J. Firstenberg, senior vice president, commercial lines

Building on strength

Although both Commercial Union and General Accident operated nationwide before the merger, each company maintained a stronger presence in certain geographic areas. "Commercial Union was dominant in the Northeast, pockets of the Midwest, and the Gulf states, whereas General Accident was strong in the mid-Atlantic, Midwest, and Northwest," Banas explains. "Combined, we now have a greater presence and critical mass in each of these key regional markets. We've moved from being a second- or third-tier player in some regional markets to first tier. The merger improves our position in personal, commercial, and specialty lines, and it significantly strengthens our agency plant."

Given CGU's combined agency force of more than 7,000, Banas observes, it's interesting that there was less than a 5% overlap in agency representation between the two insurers. The merger, he observes, has definitely created a win-win situation for agents. "The agents of both previous companies now have access to a broader portfolio of products and a broader underwriting appetite overall," he says. "Agents of General Accident can now offer their clients Commercial Union's personal lines package, as well as its agricultural and ocean marine products. Commercial Union agents gain access to General Accident's significant commercial lines appetite and its strength in surety and inland marine." As product integration proceeds over the next several months, CGU agents will be able to offer their clients an even wider array of products, Banas says.

Overall, Banas says, the merger "gave us the chance to eliminate the 'baggage' of both companies: outdated systems, procedures, products, and culture. We're building a new company by taking the best people, practices, and products from both companies, upgrading our skill set, and delivering all these improvements to our agents."

To keep its agents informed of progress on the combination, CGU regularly publishes "CGU Update" news, which informs agents on key merger issues and invites agent feedback on how the merger is affecting them and their policyholders. Response has been positive, Banas says, because agents appreciate CGU's concern for their well-being and are pleased with the company's efforts to communicate clearly and openly with them.

Aiming for first place

As a combined entity, CGU has a simple and definite objective, Banas explains. "We intend to become the premier independent agency company in the United States. We seek to earn carrier of choice position in a high percentage of our agency plant: we want to be in first, second, or third position with at least 90% of our agents." Historically, he observes, both previous companies had been focused on developing long-term relationships with agents. "CGU is now increasing its focus on building the same kinds of long-term relationships with policyholders and employees," he says. Key to this effort is the concept of retention: retention of relationships and retention of business. "Retention is so integral to our operating philosophy that everyone in our organization is focused on it," Banas remarks.

The independent agency system is CGU's sole means of distributing its products in the United States, Banas says. "We see plenty of opportunity to grow, and grow profitably, with independent agents," he asserts. "We have no reservations about independent agents' ability to sustain their position in the marketplace."

National power, regional flexibility

Delivering top-quality products and services to nearly more than 7,000 agents nationwide is a huge challenge, and one that's magnified when it's combined with the massive undertaking of completing a merger. How does CGU approach this task?

"We manage most of our business on a regional basis," Banas responds. "This way, we can focus on areas we think have the best profit potential. We operate like a regional carrier and leverage our position as an international insurer." Around the country, "We have 13 regional offices, 13 regional presidents, and 44 branch offices," he explains. "Each regional president is fully empowered to run his or her business and make decisions with little interference from headquarters. We challenge their plans, but once they're set, we work with the regional presidents to implement them."

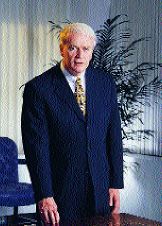

The merger of Commercial Union and General Accident has created the 16th largest U.S. insurer and a combined agency force of more than 7,000. Operating from CGU's Boston headquarters, Richard S. Banas, senior vice president, insurance operations (above), has responsibility for commercial and personal lines underwriting, claims, reinsurance and strategic planning.

The merger of Commercial Union and General Accident has created the 16th largest U.S. insurer and a combined agency force of more than 7,000. Operating from CGU's Boston headquarters, Richard S. Banas, senior vice president, insurance operations (above), has responsibility for commercial and personal lines underwriting, claims, reinsurance and strategic planning.

Centralized functions such as information technology, reinsurance, finance, and specialized technical services are performed at the home office. The functions that directly affect agents and policyholders are managed at the regional level; these are underwriting, marketing, claims, risk management, and loss control. "We're focused on meeting the needs of our independent agents, and product and service decision-making at the regional level can deliver results that aren't possible in a highly centralized operation," Banas explains. "Our regional offices have the authority and the flexibility to offer agents our broad spectrum of products, along with services that are tailored to respond to local needs."

In each regional office, commercial lines and personal lines teams are agent-focused, Banas says. "The agent can go to one team to get everything done--there's no need to go five different places. We try to keep it simple for agents and make it easy for them to do business with us."

CGU's regional operating structure, Banas believes, is a key factor that differentiates the company from its competitors. "In building on the core strengths and relationships of each company, and establishing increasing critical mass in our agency plant, we're able to create the same kind of franchise value in a wide range of regional markets as each company had previously developed in its particular regional strongholds," he explains. "Our simple operating model is different from those of most of our competitors, in the sense that it's a locally driven model with nationwide support where it makes sense. We believe we're able to offer a superior blend of products, services, and agency support, based on our tradition of integrity, stability, longevity, and accessibility."

COMMERCIAL LINES

Directing CGU's commercial lines operation nationwide is Senior Vice President David Firstenberg who, like Banas, is enthusiastic about CGU's strong regional focus. Before joining CGU in 1997, Firstenberg worked for 17 years with a large national insurer and for two years with a small regional carrier. "My two years with that company gave me a good sense of what it takes to compete in the non-big broker market," he says. "Regional companies have such great inherent potential in their markets."

In CGU's 13 regional offices, Firstenberg says, "the commercial lines managers are truly the backbone of our operation. They have the authority to establish pricing structures and develop risk selection strategies, and they're responsible for supporting our branch offices and delivering our products and services to agents." In each office, line of business managers are accountable for results in property, casualty, and workers compensation.

From mom and pop stores to mega-manufacturers, CGU writes a broad spectrum of commercial business. "Our risk appetite is quite broad--and we consider that a significant positive because it enables us to actively support our agents every day," Firstenberg says.

Agents are partners

In addition to the "three C's": character, capacity, and capital, Firstenberg says, the most important quality a CGU agent must possess is integrity. "That drives everything we do and how we do it," he says. "We want to do business with agents as trusted long-term partners." Key to the success of CGU's agent relationships, he believes, is "establishing from the start that the branch manager is accountable for delivering the entire CGU franchise to the agent. An integrated local team is in place to service the agent's needs, and we do everything we can at the home office to support that local team's partnership with its agents."

CGU is definitely a company that wants to hear from its field force, and it listens intently to what agents have to say. "We take very seriously the process of giving agents a voice," Firstenberg asserts. "At our local and regional producer advisory council meetings, agents set the agenda and say what's on their minds. I review the minutes of each meeting to identify the open action items; this helps me keep in touch with what's happening in the field." One agent from each of the company's 13 regions serves on a national producer advisory council. This group, which is divided into subcommittees for personal lines, commercial lines, and agent relations, meets twice a year, again with agents setting the agenda.

A particular source of pride at CGU, Firstenberg says, is its strong support of education for agents. The company sponsors a four- to six-week school for agents who are new to the business or new to personal or commercial lines. "It's a great way for us to build long-term relationships with people who are just coming into the business," he notes, "and it gives them an edge in product knowledge." Insurance school isn't cheap, he acknowledges, but "In an expense-conscious era, we think of education as an investment."

Asked how he would describe CGU's relationships with its agents, Firstenberg responds, "Solid, strong, and mutually supportive. Since the merger, I sense a really striking desire among the field force for us to succeed, and I think this reflects our true commitment to the independent agency system."

"Given our underwriting strength and supporting services, and our broad risk appetite, we have no apprehension about working with agents on higher-hazard risks."

"Given our underwriting strength and supporting services, and our broad risk appetite, we have no apprehension about working with agents on higher-hazard risks."

--Jack Doyle, senior vice president

SPECIALTY LINES

As the result of the merger, CGU boasts a strong and growing specialty lines operation that's currently producing about $500 million in premium volume. Under the leadership of Senior Vice President Jack Doyle, a 35-year veteran of General Accident, the specialty business division focuses on surety, ocean marine, inland marine, global and national accounts, and national programs. The division also offers a variety of custom programs both nationally and regionally.

The specialty business units operate under a relatively flat organizational structure, Doyle says. From the home office, he provides leadership to CGU's eight specialty business units located throughout the country. These units were not relocated as a result of the merger so as not to cause disruption in their operations. Describing his responsibilities, Doyle says, "I work with the specialty business leaders to help them implement their operating plans. They're highly skilled experts, and they don't need a lot of bureaucratic intervention."

Like Firstenberg in the commercial lines division, Doyle finds CGU's strong regional network an invaluable asset in building specialty business. "I rely heavily on our regional offices; they're key players in marketing our specialty capabilities," he explains. "We count on them to lay out the broad capabilities of the CGU franchise and to provide feedback that helps us market our products effectively."

Holistic approach

"In the specialty business, we've found that the key to success is to build underwriting expertise and combine it with differentiated products," Doyle says. "We favor a holistic approach that brings together products, underwriting, loss control, claims, and quarterly account reviews. This allows us to give our agents and brokers something different to sell that will help them sustain their competitive advantage." To identify customer needs and tailor coverages that meet those needs, his division conducts policyholder focus groups. Agents are very much a part of this effort. "We form a team that includes the agent or broker," he explains. "We consider them an extremely valuable resource."

Like Firstenberg, Doyle emphasizes the importance to CGU of establishing and maintaining solid, long-term relationships with producers. "It's the culture of both companies to maintain a more interpersonal relationship with agents and brokers than some of our competitors," he comments. "We look at the longer term. Some companies overlook the value agents and brokers can bring to the insurance sale. We really view them as a resource to help us meet our policyholders' needs."

In specialty lines, some insurers prefer to work only with producers who have in-depth knowledge of a particular area. Not so at CGU, Doyle declares. "Given our underwriting strength and supporting services, and our broad risk appetite, we have no apprehension about working with agents on higher-hazard accounts." What's more, "CGU has a business development unit whose task is to create new opportunities in products and markets. In the specialty division, as we move into the future, we'll be working with agents in designing solutions to meet policyholders' needs. Increasingly, producers will play a vital role in our effort to deliver new products and services to our insureds. A key benefit of the merger is that it gives us even more opportunities to support our agents and brokers."

PERSONAL LINES

In addition to commercial and specialty business, CGU is a strong force in the personal lines market. Operating under the direction of Senior Vice President William Rockenstein, a veteran of Continental Insurance and then Commercial Union, CGU's personal lines operation is modeled on Commercial Union's highly successful personal lines center organization, which Rockenstein says was extremely efficient from an expense standpoint. A major challenge after the CU-GA merger, he observes, was forming nine personal lines centers out of the previous 42 underwriting locations. "Each of the company's 44 branches, however, has primary responsibility and accountability for managing the personal lines business in its territory," he explains. "This keeps us closer to our agents, and we can achieve efficiencies by underwriting and servicing business in our nine personal lines centers. Our employees spend a lot of time talking to agents."

As in commercial and specialty lines, CGU's appetite for personal lines risks is broad, Rockenstein says, and product offerings include a number of special programs. "We have both internal and external views of our business," he explains. "From an external perspective, our goal is to satisfy the customer's lifetime insurance needs. Internally, we focus on the customer's lifetime value to us. We treat all of our customers exceptionally well, but we reward them differently based on profitability. The breadth of our underwriting appetite is relative to the length of time we expect to retain a customer. Customer retention drives everything we do

in personal lines."

Among CGU's personal lines products are the Custom-Pac, a combination homeowners and personal auto policy; the Prime Time Plan, created for insureds over age 49; and the Financial Rewards Plan, for insureds who have an exceptionally good credit rating. A primary focus, Rockenstein says, is to "develop additional markets that deserve special rewards. Profitability underlies our approach."

At CGU, having a broad risk appetite in no way means taking on all comers. "We never intend to offer the lowest price or the broadest coverage," Rockenstein says. "With our strong agent relationships and our excellent underwriting, claims handling, and other services, we strive to deliver to the policyholder a complete package--what we call 'the best total solution.'"

Focus on retention

Asked how he views his division's relationships with producers, Rockenstein responds firmly, "Our independent agency relationships are everything to us. We live and die on how strong they are. To us, retention doesn't refer only to policyholders; it also encompasses our associates and our agents. Our policyholder relations go through the front and back doors of our agents. We don't intervene unless we can complement what the agent is providing. We're looking for long-term agency relationships that are a two-way street, where we establish a set of mutual objectives that we focus on. We like to work with agents who focus on personal lines, who are knowledgeable about the marketplace, who understand customers and their expectations, and who are aware of how we can help them." Another important attribute CGU seeks in an independent agent, Rockenstein notes, is technological awareness coupled with receptivity to the changes automation brings.

What kinds of services and support does CGU offer the agents through whom it writes personal lines business? "We're constantly looking for ways to help agents produce new business," Rockenstein responds. "We give them leads for our target markets, such as the Financial Rewards Plan. We also offer an array of interface options." He notes, however, that "Our profitability, and that of our agents, is driven less by new business than by retention, so we try to keep our focus there. Looking at retention helps us identify what customers we want to keep, whom we want to work with over time in partnership with our independent agents, and how we can best meet their needs." This approach, Rockenstein emphasizes, supports CGU's commitment to being the "best total solution."

The CGU advantage

If there's such a thing as a marriage of equals, it appears to be taking place at CGU as two strong, market-leading insurers come together to share the best each has to offer. "As we evolve, CGU's unique advantage is leveraging the legacy and business strategies of its predecessor companies," says Robert Gowdy, CGU's president and chief executive officer. "CGU is drawing upon the best of our prior resources to create products, services, and operating efficiencies better than either company had individually. Our future looks very promising as we begin to capitalize upon the merger's benefits, particularly as regards new opportunities for our agents, brokers, and policyholders." *

The author

Elisabeth Boone, CPCU, is a copy manager for a major health sciences publisher based in St. Louis. She is a former member of the editorial staffs of Best's Review and American Agent & Broker.

©COPYRIGHT: The Rough Notes Magazine, 1999