BRIGHT IDEAS FOR

FINDING AND FINANCING

BRIGHT IDEAS FOR

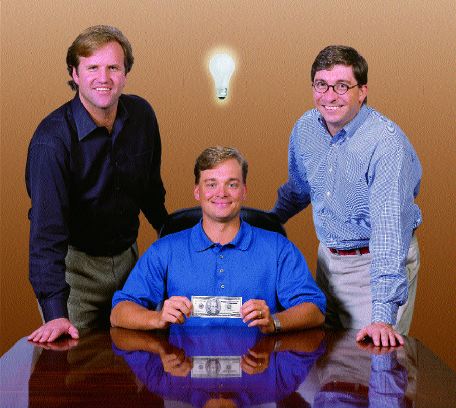

General partners of Tobat Capital, LLC, are (left to right) Cory L. Moulton, Scott T. Brock and Ian D. Packer.

By the time you read this, Tobat Capital, LLC, will be up and running. Running what? Running an innovative investment firm, with $100 million in venture capital, aimed at combining the power of the Internet with the power of insurance.

Tobat, based in Dallas, is the creation of entrepreneurs and venture capitalists. Specifically, it's the brainchild of three executives from E.W. Blanch Holdings. The General Partners of the company are men who left Blanch specifically to form Tobat: Scott Brock, who's been active in strategic insurance investments and acquisitions; Cory Moulton, who headed international reinsurance at Blanch; and Ian Packer, former chief financial officer at Blanch and a man with working experience in both merchant banking and insurance.

When Rough Notes talked to Packer, he explained how the company intends to make strategic investments in companies that can make Tobat investors wealthy--and the insurance industry efficient.

Packer and his partners formed Tobat after sizing up the $1.2 trillion marketplace that the insurance industry represents. They believe that the financial services industry has been slow to adapt to technological and distribution advancements, estimating that distribution costs in insurance alone exceed $100 billion annually. From a business-to-business perspective, they believe a lot of those costs can be pulled out of the industry, once insurance companies understand and adopt several new solutions.

Tobat will focus its investments on business plans that are targeting three of the industry's most significant challenges:

* Flat growth

* Antiquated legacy systems

* High distribution costs

Some of the problems facing the insurance industry are a combination of challenges. For example, what about term life insurance? Packer believes that before long, low-level policies of, say, $250,000 or less will be underwritten and "Jet Issued" directly over the Internet without going through a lengthy application process.

"You can issue the policy right now," said Packer. "That's important because people want fulfillment when they decide to buy."

Packer is quick to note that Tobat won't be selling these policies; rather it will merely be investing in companies that possess the technology or distribution solution to accomplish such a task.

"We're the financier of the enabler," Brock said of Tobat.

|

|

|

In their quest to move to just-in-time (JIT) inventory systems, the auto and aircraft manufacturing industries already have adopted business procedures that could be reshaped to fit the claims processing system, rather than try to build new technology from the ground up, said Packer. One of Tobat's potential investments is developing a plan to target this exact opportunity.

"We think of ourselves more as applied technology experts as well as inventors," said Packer. Tobat will be making equity investments in companies that have begun operations. They may not be household names, but they've gone beyond the blueprint stage and are beginning to sell their goods or services in the marketplace. In order to qualify for review by Tobat,

they'll be expected to show that within 18 months they can generate $20 million in annual revenues, and $250 million in within five years.

In general, Tobat will focus on companies and business plans that are utilizing technology to streamline distribution costs and enhance operations. This is broken down further to companies that offer either B2C (business-to-consumer) products, or B2B (business-to-business).

* B2C through B2B affinity group distribution

* B2B e-commerce "enablers"

* Business process outsourcers

* Virtual insurance company applications

Moulton makes it clear that Tobat will tread carefully as it moves into B2C enterprises. Investing in companies that plan to maintain an expensive Web presence to try to sell high-value insurance policies, for instance, is a flawed strategy, in his opinion.

"Consumers may go there once a year," he said. "Insurance is not a sell, like books."

Packer also is aware that many B2C e-commerce sites have crumbled within the past few months. There have been some spectacular downfalls, with health care, retailing and even some insurance Web sites drastically retrenching or simply folding their doors.

While B2C business opportunities may require especially tough inspection, Tobat is very comfortable with developments in B2B. Research indicates that literally trillions of dollars worth of goods and services will be traded via the Internet. So, while Tobat may not want to sponsor companies that operate portals, it wants to invest in companies to develop software and other computer applications that enable insurance companies to post their own. Further, it wants to introduce to the market products that will allow insurers to rate, quote and issue policies more efficiently.

"Big insurance companies aren't especially interested in running all this stuff," said Brock. That means they'll search out vendors who are specialists in the field, and who can keep current on the rapid pace of technological change.

Moulton pointed out reinsurance as an area of opportunity. That business has yet to be significantly impacted by the e-commerce revolution, he noted, but he believes "the wave is reaching a crescendo."

"Over the next 18-24 months," Brock predicts, "thousands of Internet financial services companies will participate in a 'land grab' similar to that already seen in other consumer products sectors." Perhaps Tobat managers were thinking of the securities market revolution, where e-commerce has pushed transaction costs to mere pennies and made the market accessible to millions of people who might otherwise have stayed away.

Packer and his partners formed Tobat after they saw a lack of venture capital focusing on the insurance and reinsurance industry. Where others saw problems, they saw opportunities. As Tobat pointed out in its private placement memorandum of earlier this year, "Many traditional financial services companies are characterized by inefficient infrastructure with flat growth rates, antiquated technology and cumbersome distribution models." The solution is to provide those companies with e-finance solutions that "revolutionize these areas through new technologies, increased productivity and dramatically lower cost structure."

Tobat has attracted some heavy hitters as investors. Their investors consist of both domestic and international insurance companies, money managers and high net worth individuals. Tobat considers its institutional investors as important strategic pieces to the puzzle because they will be the first to test and qualify a majority of these new innovations.

Already, Tobat has looked at more than 120 business plans and is ready to review more. After jumping through exhaustive internal due diligence hoops, it will whittle that list to around 10-12 investments.

Typically, Tobat will invest $5 million-$10 million, perhaps as much as $15 million in a venture over time. It will take an equity stake in exchange for its cash infusions and hopes to eventually help guide each of those companies to a successful exit strategy, either a sale or initial public offering (IPO). Its goal is to create internal rates of return on capital in excess of 25%.

Tobat does not have the field entirely to itself when it comes to such a fund. Other companies also are pouring cash into modernizing the delivery of financial services. But Brock said he believes that Tobat has defined its focus sharply enough--especially in its concentration on young companies in the insurance or reinsurance field--so that it won't duplicate the efforts of anyone else.

Packer also said that Tobat would execute its business philosophy in a way that won't be a threat to independent agents. Indeed, its aim is to help insurance companies, which in turn will help agents by allowing them to offer a more competitive product.

"If we get a better claim resolution (system), that just adds to the quality of service that the agent can provide," he said.

Though the phrase is in danger of becoming overused, the success of Tobat could be a win-win-win-win. Investors gain, insurance companies gain, insurance agents gain, and their clients gain.

"A few years from now, we want Rough Notes readers to say, 'Hey, that's the company that re-shaped the entire insurance industry,'" said Packer. *

For More Information

Tobat Capital, LLC, 4308 Avondale, Suite 200, Dallas, Texas 75219, (214) 219-8080