Drought-induced losses prompt more widespread mitigation efforts

By Brett Hanavan

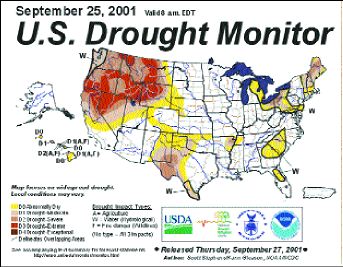

Map courtesy of National Oceanic and Atmospheric Administration

Actuaries, historians, land use planners, farmers, and naturalists agree that wildfire is a renewing natural act designed to replenish and restore the landscape. However, they--along with the insurance industry--also recognize that if wildfires get out of control, they can quickly become catastrophes. Growing suburban development, with its increasing number of rural dwellings, has exacerbated the potential for destruction.

During this past summer, wildfires burned a total of 3,048,769 acres (through September 17). The largest loss to private structural property occurred in California on September 7, when a fast-moving wildfire raged through the Sierra Nevada foothills 85 miles north of Sacramento. It consumed about 40 homes, 152 outbuildings, 146 vehicles, and two rural businesses. Called the Poe Fire, it took seven days to contain, burning 8,333 acres and causing 22 injuries.

The Poe Fire was caused by a tree falling into a power line and, like so many others, it moved fast, feeding on wild brush fuel. The fire moved across the land so fast that those who were prepared still didn't have time to flee with much more than the bare essentials. It came at a time when red flag warnings were posted and winds of 10-15 mph pushed to gusts of 25 mph with little relative humidity. Fire ignition raged quickly that morning, and weather elements caused the Poe Fire to ignite an unprecedented 20 to 100 acres simultaneously.

"This area of the earth is comprised of low brush, oak grass, and young mixed conifer," says Janet Marshall, public affairs officer of the California Department of Forestry (CDF Fire), which oversees fire fighting in this rural area. "It is an urban interface area and overall 400 homes were threatened."

Marshall points out that urban interface is quickly becoming a concern among wildfire management experts, as people from major population centers move into upscale homes in rural, often more isolated, areas. It is common in areas of eastern California where people move to more rugged, wild lands and are building homes in brush and thick timber. This poses problems for insurance underwriters and agents who seek to properly manage brush exposure within their books of business.

In the northwestern portion of California, Darlene Penfold, principal and manager of Penfold-Leavitt Insurance Agency, an independent agency in Eureka, California, says that her agency has not seen much of a change in rates.

"It is more of a tightening of underwriting requirements," Penfold said. "This pertains to any indication of brush in the vicinity of a home as well as location as pertains to a responding fire district."

Penfold-Leavitt maintains a spread of about 65% commercial business and 35% personal lines business. Of the 35%, about one-half is homeowner and/or dwelling fire business.

"There have been a few circumstances where we have worked both with the carrier and the insured to be sure that brush is cleared around or near a building for protection in the event of a forest or brush fire," Penfold adds. "Occasionally we also work with an insured in an advisory capacity regarding other protective measures that can be accomplished, such as the installation of a pond or other source of water near a home."

Wildfire losses, in the West and elsewhere, are not a new phenomenon, although severe drought conditions of the past two summers have brought them into the spotlight. In 1991 a fire in the Oakland Hills area of California resulted in the destruction of 2,331 structures. The fire occurred largely in an area of dense brush, rolling hills, and high-dollar custom homes.

Now, 10 years later--from the ashes of this loss--has come a more formalized damage inspection process designed to help reduce future losses. Ethan Foote, the CDF Fire's Butte County battalion chief says the post-loss inspections include building construction, access to property, and vegetation clearing. "Still one of our biggest considerations is the amount of untreated roofing material still in use on structures in California. Now, all wood shake must be treated or not used."

Although such measures help mitigate ultimate loss, the threat of fire itself continues. This summer's fires in the West occurred over wide areas. A September 17 report from the National Interagency Fire Center (NIFC) in Boise, Idaho, said fire danger indices were "very high" to "extreme"--in Arizona, California, Idaho, Montana, Nevada, Oregon, Utah, Washington, and Wyoming.

Losses have included not only property, but lives. On July 10, four eastern Washington firefighters were killed and four others injured while fighting a wildfire that burned 9,300 acres in the north central region of the state. In California, two air tanker planes collided while fighting wildfires, killing the plane's two pilots.

In the early 1990s, following the Oakland Hills fires, theories began to change about how to manage wildfire. Aggressive suppression management was no longer the buzz-word by 1999. According to the Environmental News Network, decades of suppression have led to wildfires that have become progressively bigger and more expensive while damaging the eco-systems that are dependent on fire.

New technologies in predicting forest conditions have allowed "cool fires" to be lit regularly to purge combustible fuel loads in forests and grasslands. Many fires are allowed to run their course on National lands or in government property situations, returning the earth to conditions under which it thrived for millions of years prior to civilization.

As part of this management effort, the U.S. Forest Service says it currently approaches mitigation by reducing fuels around communities first--thinning small trees that crowd forest undergrowth. It does this in areas near watersheds that serve as sources for fighting wildfire. The Forest Service is implementing this technique in

1.8 million acres this year. More thinning is planned in 2002. Some authorities and naturalists say that the thinning plan goes way too far, as unnecessary trees are cut down in far too wide an area.

Carrier concentration in the fire-prone West

For insurance companies, a large portion of the exposure to the wildfire risk in seven fire-prone Western states is concentrated in a few carriers. According to Weiss Ratings, eight large property/casualty insurers cover 74.5% of the home insurance risks in these states. Weiss Ratings issues financial and safety ratings on more than 15,000 financial institutions, including property and casualty insurers.

A Weiss report states that at year-end 2000, these eight carriers' percentages of the market were as follows:

State Farm Group: 22.4%

Zurich Financial Services Group: 18%

Allstate Group: 15.4%

Safeco Group: 5.8%

USAA Group: 4.4%

California State Auto Group: 3.8%

Allianz: 2.4%

Automobile Club of

Southern California: 2.3%

The common factor in agency and book management of wildfire exposure is not to write bundles of homes in potentially high brush fire exposure areas; also, to avoid placing them all within one carrier or program. On an individual risk basis, agents can help assure that exposure is minimized in regard to structures by assuring that there is adequate clearing of wild brush within 50 to 100 feet of dwellings and outbuildings; proper, non-combustible ground cover is planted and growing in that space; and proper roofing material is used. *