John Kessock, Jr., chairman (seated), and Richard Turner, president, Commonwealth Risk Services.

![]() ot so long ago, the alternative insurance market seemed somewhat like alternative music: complex, edgy, intriguing--and perhaps a bit intimidating. Evolving to fill the gaps left by the severe market crunch of the mid-1980s, the alternative market was viewed by many as a temporary haven from wild swings in the underwriting cycle--not as a permanent solution to the challenges of financing risk.

ot so long ago, the alternative insurance market seemed somewhat like alternative music: complex, edgy, intriguing--and perhaps a bit intimidating. Evolving to fill the gaps left by the severe market crunch of the mid-1980s, the alternative market was viewed by many as a temporary haven from wild swings in the underwriting cycle--not as a permanent solution to the challenges of financing risk.

That was the popular wisdom several years ago. Since then, the alternative market has quietly been expanding in both reach and volume, to the point where today it rivals the traditional property/casualty market in premiums written. No longer the exclusive province of the Fortune 500 and mega-brokers, the alternative market increasingly is becoming the vehicle of choice for a wide range of agents and brokers and the clients they represent.

A driving force in shaping today's responsive and sophisticated alternative market unquestionably is Commonwealth Risk Services, the U.S. sales arm for the products and services of the Mutual Risk Management Ltd. (MRM) family of companies. From its headquarters in Philadelphia, Commonwealth Risk works with agents and brokers to forge creative solutions to their clients' complex risk financing challenges. Over the years, Commonwealth Risk has developed an impressive body of resources and expertise that place it squarely in the forefront of alternative market innovations.

Focus and commitment

Founded in Hamilton, Bermuda, in 1977, MRM conducts operations through more than 30 subsidiaries; these consist of service companies

(of which Commonwealth Risk is one) as well as facilities for specialty brokerage, captive management, rent-a-captives, policy issuance, and financial services. MRM is organized into four business segments, each of which is accessed through Commonwealth Risk's sales representatives.

"Our programs are wide and diverse. There's no 'typical' program."

"Our programs are wide and diverse. There's no 'typical' program."

--Richard Turner, President, Commonwealth Risk Services.

1. Program Business. In program business, which constitutes more than 50% of MRM's fee income, Commonwealth Risk brings together producers and reinsurers of specialized books of business, both of whom may assume risk and share in underwriting profits and investment income. The book of business may include a select group of insureds, a formal association of like insureds, or virtually any industry class or niche an agent chooses. Program business can accommodate property and casualty as well as accident and health lines of business.

2. Corporate Risk Management. This segment of MRM's business provides services to businesses and associations that wish to insure a portion of their risk in a loss-sensitive alternative market structure. Using MRM's offshore captive expertise, Commonwealth Risk's founders pioneered rent-a-captive solutions they later trademarked as Insurance Profit Center® (IPC) programs. Ideally suited for premiums of $750,000 or more, IPC programs can be established for individual mid-sized corporations in a range of industries, including transportation, construction, manufacturing, wholesale/retail, financial services, agriculture, and health care. For associations, IPC programs can be created that enable smaller insureds to enjoy financial advantages usually available only to larger accounts: unbundled services, access to managed care, and the return of underwriting and investment income. The MRM companies also offer wholly owned captive management facilities in Barbados, Bermuda, Cayman, Dublin, Guernsey, and Vermont, and assist captives with support services that include policy issuance, feasibility studies, registration, filings, legal requirements, and ongoing management.

3. Specialty Brokerage. Commonwealth Risk offers access to MRM Specialty Brokerage Ltd., which in turn is a conduit to large capacity and major catastrophic insurers and reinsurers in Bermuda, Europe, and North America. Both treaty and facultative coverages are available, with access to large capacity captive, rent-a-captive, and other property and casualty programs worldwide.

4. Financial Services. Commonwealth Risk affords access to MRM's newest business segment, which handles private client trust and administration services, manages a proprietary family of offshore mutual funds, administers offshore funds, and provides asset accumulation life insurance products designed for high net worth individuals.

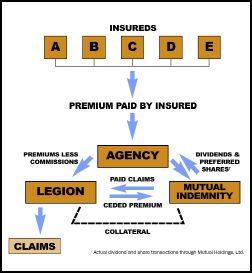

Until 1987, most of MRM's program business and other placements were handled through major national insurers. That year MRM acquired what now is known as Legion Insurance Company. Operating as the Legion Companies, Legion Insurance and its affiliates, Villanova Insurance and Legion Indemnity, provide both admitted and nonadmitted markets for MRM clients who want to structure alternative risk financing programs. The Legion Companies issue policies to insureds. The risk is then shared by any combination of the Legion Companies, the insured or other investor, and nonaffiliated reinsurers. Each of the Legion Companies is A rated by A.M. Best and A+ by Standard and Poor's for claims-paying ability.

Tough market, bold solutions

Tough market, bold solutions

Commonwealth Risk was founded in 1984 by MRM Executive Vice Presidents Richard Turner and Glenn Partridge. "The timing of Commonwealth Risk was dramatic," comments Reginald Pierce III, senior vice president of marketing and communications. "We opened our doors right at the beginning of the hard market in 1985."

At that time, traditional insurers that for the past several years had presided over a freewheeling competitive frenzy were starting to sober up as they contemplated the staggering losses on the business they had slashed rates to acquire. Capacity shriveled, policy terms stiffened, and prices skyrocketed as carriers struggled to regain their equilibrium. The party clearly was over, and the doors were slammed shut on stunned agents and insureds.

Into this arid landscape the alternative market was born. Companies like Commonwealth Risk and MRM became laboratories for experiments that would forever change the chemistry of the property/casualty insurance market. Drawing on their expertise in using offshore markets to structure rent-a-captives, Commonwealth Risk and MRM were able to craft creative solutions for risks that had never ventured outside the confines of the traditional market.

Initially the alternative market was viewed by many as a desperate fix for a temporary problem, and as a mechanism that would wind down when the tight market began to loosen up. In the early 1990s traditional insurers did indeed reopen their doors, display their lavish stock of wares, and roll out the welcome mat. Many insureds that had turned to the alternative market found themselves unable to resist the lure of limitless capacity at bargain prices. But a funny thing had happened during the dark days of the 1980s: vast numbers of insureds that had turned to the alternative market in desperation realized that it offered benefits that were unavailable in the traditional market: stability, claims reduction, profit participation, and control.

Flexible and innovative

Certainly Commonwealth Risk and MRM had to respond to the new surge of competition from the traditional market. "In some cases we do things in the same way we did them in 1984 and 1985," Turner acknowledges. "But we've also branched out by offering Agency IPC programs and association captives to smaller risks." While continuing to structure risk financing packages for large corporate risks generating premiums between $500,000 and

$5 million, Commonwealth Risk and MRM now use many of the same strategies to address the needs of smaller entities that want to participate in their own risks.

Commonwealth Risk executives (from left) John T. Naughton, CPCU, senior vice president, Andrew A. Lewis and Jerry Rivers, executive vice presidents; Jeffrey A. Packard and S. Alan Pesolyar, senior vice presidents.

Commonwealth Risk executives (from left) John T. Naughton, CPCU, senior vice president, Andrew A. Lewis and Jerry Rivers, executive vice presidents; Jeffrey A. Packard and S. Alan Pesolyar, senior vice presidents.

"As some of our Agency IPC programs started to grow, we looked to offer their facility through other agents and brokers," Turner says. "For example, we were approached by an agent who specializes in golf clubs and helped him open up his program to agents and brokers in other locations." Program business now accounts for more than half of Commonwealth Risk's fee income. "Our programs are wide and diverse," Turner comments. "There's no 'typical' program. Some are offered through managing general agencies (MGAs) and others through agency captives. We use our three affiliated insurance carriers to develop appropriate coverages and filings." Although not all of Commonwealth Risk's programs are open, Rivers notes, "many can be accessed by retail agents through our www.accessMRM.com Web site, toll-free fax-on-demand system, and Pocket Finders guide."

Unlike competitors that must accept the terms and conditions of outside insurers, Commonwealth Risk offers insureds the advantages of access to MRM's own family of carriers, the Legion Companies. "We use creative applications of our rent-a-captive as a locomotive to drive the process," Turner explains. "This allows us to attract agents and brokers by offering diverse products to meet their clients' needs, and to differentiate ourselves from competitors. We have a sales force that pursues deals instead of waiting for them to come to us. Targeting the business we want gives us an advantage with selection, and having access to our parent company's insurers means we can package deals quickly."

One-stop shop

At Commonwealth Risk, there's a keen awareness that whatever the size of an account, the quality of the business depends to a great extent on the skill and expertise of the agent or broker. "We pride ourselves on working with agents and brokers; they're our bread and butter," Pierce asserts. "We want to be agents' source of knowledge and expertise in the alternative market," Rivers adds. "We want agents to think of us when they think of rent-a-captives and large deductible programs. We want to be the agent's partner. An agent or broker might know that a company has a market for a certain product but have no idea how to gain access to it. The agent can make one call to a Commonwealth Risk sales representative, and we can take it from there. From a large corporate risk to a smaller agent, we offer complete one-stop shopping."

Andrew C. Cavenagh, senior vice president at Commonwealth Risk's San Francisco office.

Andrew C. Cavenagh, senior vice president at Commonwealth Risk's San Francisco office.

Although Commonwealth Risk excels when sitting across the table from large corporate clients and mega-brokers, Turner emphasizes, "Most of our business is not done with the Aons and Marshes. The vast majority of our business comes from regional brokers and independent agents and brokers. We want to work with agents who have strong relationships with their clients. We sell quality and value, not price. The agent should understand the client and want to find the best solution for the client's needs, rather than focusing on getting the lowest price."

If price is the only consideration, Commonwealth Risk isn't always the answer, Turner adds. "We have a strong history of attracting quality agents and brokers, and we like to develop long-term relationships with them. We act as a consultant to help the agent develop solutions to meet the client's needs. We're not a quick fix for price problems."

Marketing makes the difference

Both Program Business and Corporate Risk Business are spearheaded by Commonwealth Risk's producers, Rivers says. Once Commonwealth Risk has designed a new program, its field marketing department, headed by Vice President Richard Look, steps in. "Rich Look's department provides a menu of value-added services to MGAs and agents and brokers," Rivers comments. "Our field marketing operation has some unique aspects," Pierce adds. "Many MGAs are good at their individual niches, but they may lack the time or resources to develop a marketing plan. Our field marketing department puts together a marketing plan for them. We increase our retention of MGAs and agents and brokers by enhancing our relationship

with them."

Michael C. Mutascio and C.A. (Tripp) Craig, senior vice presidents.

Michael C. Mutascio and C.A. (Tripp) Craig, senior vice presidents.

An essential element of Commonwealth Risk's marketing strategy is its five regional sales teams, each of which is headed by an experienced team leader. "Our team leaders' responsibility is to meet the year's new business goals and serve as mentors to the salespeople who report to them," Rivers explains. "The team leader system works well in training new producers and maintaining esprit de corps. The team approach definitely adds value to our agents and brokers." Teams don't compete with each other at Commonwealth Risk, Turner adds, but freely share their experience. "We encourage cross-pollination among our teams. For example, our East Coast producers might spend a week with our West Coast producers to exchange information and ideas."

At Commonwealth Risk, there's keen appreciation for the contributions of seasoned producers, and pride in retaining them; the average producer has been with the organization between five and 10 years. "Our producers work well with the agency community. They understand agents and can access products and services that add value," Turner says. "Our producers offer to assist agents with presentation materials, to provide a comfort level that helps the agent handle the situation with the confidence of being supported by our in-house resources. Most people don't like to buy insurance. We want to make it a positive experience." Adds Rivers: "Our producers can help direct the agent toward the best third-party administrator or loss control specialist in his or her area."

Jerry Rivers, executive vice president of Commonwealth Risk Services.

Jerry Rivers, executive vice president of Commonwealth Risk Services.

--Jerry Rivers

Opportunities abound

Commonwealth Risk has the expertise and flexibility to adapt to changing market conditions. "During the soft market, our Program Business expanded rapidly, though we expect to see this segment flatten as programs that do not produce an underwriting profit are unlikely to survive," Turner remarks. "However, our Corporate Risk sector will benefit dramatically from a harder market."

The firming market is warmly welcomed by Commonwealth Risk. "In 2000, we saw a 21% overall increase in submitted Corporate Risk business after three flat years," Pierce observes. "We're very excited about the future." Sharing Pierce's optimism, Turner says, "With a return to sense in the market, we see opportunities abounding. It's a great opportunity for agents to use our approach for their clients with more than $500,000 of premium. Through agency-owned captives and rent-a-captives we can provide the tools to keep claims down, control costs, and generate investment and underwriting income. This is an exciting time, and we have the demonstrated ability to help agents take advantage of it. In today's hardening market, agents and brokers should take notice of Commonwealth Risk."

Whether the insurance market is hard, soft, or somewhere in between, Commonwealth Risk is confident of its ability to succeed by devising innovative solutions to risk financing challenges. "What we bring to the table is intellectual capital," Rivers asserts. "We've been through all the market cycles, and we've always managed to stay a step ahead. Through MRM, we have access to insurance, policy issuance, and rent-a-captive facilities. There's a lot of value in controlling those resources, and in being smaller. We're not too big to be flexible and responsive to change. We've grown over the years, but we still operate as entrepreneurs."

In an era when the consumer is widely regarded as king, Turner observes, insurance seems to be a notable exception. "We tend to think we're in an industry that is not always responsive to customers. We see ourselves as the 'uncola.' We try to do things differently from conventional insurance companies with their bureaucracies and red tape. We try to differentiate ourselves by creating individual solutions instead of using a 'one size fits all' approach. We're a customer-driven company, and our customers are our agents and brokers. We pride ourselves on thinking outside the box and delivering solutions that make sense to the agent and its client." *

For more information:

Commonwealth Risk Services

One Logan Square, Suite 1500

Philadelphia, PA 19103

Phone: (215) 963-1600

Web site: www.accessMRM.com

Fax-on-demand: (800) 454-4525