BANKS AND INSURANCE AGENTS

A marriage made in ...?

By Dennis Pillsbury

"Community banks and independent agencies are very similar in the way they serve their community," says Jim Campbell, senior vice president and principal, Reagan Consulting, Atlanta. "Both are very community oriented and have strong, intimate customer relationships."

It is for this reason that "once smaller community banks get into the insurance business, they are often better at it than the larger banks." What makes that so ironic is the fact that it has been the larger banks that have successfully led the charge into the insurance business. In the most recent "Study of Leading Banks in Insurance," Reagan Consulting and the American Bankers Insurance Association (ABIA) found that the eight banks identified as bank-insurance leaders were predominantly larger banks. "The larger banks are disproportionately represented among those that are successfully integrating insurance with other services," Jim notes. Reagan has conducted the study for four consecutive years and will continue doing it on an annual basis. It originally was commissioned by the Association of Banks-in-Insurance (ABI) which merged with the ABA Insurance Association (ABAIA) on March 31, 2001, to form the ABIA.

The current study looked at the year 2000. It found that, for the first time, "community banks are making real progress in this effort to offer insurance to their customers," Jim points out. "They're still trailing the larger banks but are moving up and closing the gap." The study is designed to look at three aspects of the banking and insurance integration. The first objective is to develop a good macro view of the bank insurance industry. The second objective is to try to understand what strategies they are pursuing. And the final objective is to identify the banks that are leaders in the field and determine what distinguishes them.

The current study looked at the year 2000. It found that, for the first time, "community banks are making real progress in this effort to offer insurance to their customers," Jim points out. "They're still trailing the larger banks but are moving up and closing the gap." The study is designed to look at three aspects of the banking and insurance integration. The first objective is to develop a good macro view of the bank insurance industry. The second objective is to try to understand what strategies they are pursuing. And the final objective is to identify the banks that are leaders in the field and determine what distinguishes them.

Jim explains that it was not surprising that the smaller banks were trailing the larger banks since for them "it was a more complicated conundrum. They don't have all the options available to them as the larger banks. They don't bring the same level of cross-selling leverage, for example. Some have overcome these obstacles by establishing consortiums of community banks," he says.

Long-term commitment is key

While the study found that there was "a real diversity in the strategies employed by the successful banks," Jim says, "there was one common theme among all of them--they viewed the entry into insurance as a long-term objective. They were not simply looking for non-interest income but viewed insurance as strategically relevant in their endeavor to provide more integrated solutions to their customers." This long-term view is especially important since "the reality is that in the short term, insurance does not provide a great amount of income."

He points out that this follows a general change in the way banks do business. "In the past, banks really provided an inventory of products. Today, they have become advisors and, under this new model, they can't really afford to leave out an important part of the financial puzzle--insurance protection."

"We also saw that the leading banks were doing a better job at follow through," Jim continues. "They didn't stop once insurance was introduced, but made insurance distribution part of the culture at the bank." This included training bank personnel on cross-selling insurance and compensating them for doing so. "It's not enough just to send out the memo that says: 'We're now in the insurance business,'" Jim comments, pointing out that it seems like for many banks, "getting into insurance was on their 'to do' checklist and once they checked it off, it was over."

Agents remain the principal distribution channel

Although banks use a number of different distribution systems, the study found that "agency acquisitions are the preferred platform for property/casualty and benefits," Jim reports. "The de novo approach was common for individual life and health products." He continues, "[M]ost banks now are starting with: 'Is the right agency available?' They've gotten a lot smarter in terms of what they're looking for. They want a foundation on which they can build--and that's an agency with principals and producers who are planning to remain in the business. The banks look for successful, growing agencies and treat them much more like partners, giving them the autonomy they need to continue to succeed. The new strategy is to get the best and let them do their thing while finding ways to push business towards them."

Vernell Hogan, managing director, Bankers Insurance, LLC, Richmond, says that her company was "looking at agencies in Virginia that had been in business for a number of years and offered growth, profitability and good retention ratios. We weren't looking for agencies where the owners had an exit strategy." Bankers Insurance was formed by a consortium of 58 community banks in Virginia and is managed by the Virginia Bankers Association. The company worked with Reagan Consulting on a plan to enter the property/casualty business.

Vernell, who has worked with the Independent Insurance Agents of America, says she was struck by the commonalities between community banks and independent agencies. "They both have a strong connection with their customers and are interested in adding value for their customers."

Bankers Insurance acquired its first independent agency in October of 2000, closed on three more January 1, 2001, and added one more in October of 2001. "These agencies and their branch offices were spread across the state. We were looking for a geographic spread that matched that of the banks in our consortium."

A very considered approach

"We decided to take a very systematic approach to our entry into the insurance business," Vernell says. "We officially opened our doors on January 1, 2001, but that actually involved a meeting with the management advisory committee (consisting of the principals of the acquired agencies) to develop their input into the master plan we had created. We continued to meet monthly and around April or May began holding regional meetings for the senior people of the banks to explain our decision to focus on each bank's core group of customers."

Vernell continues that their objective was "to bring the expertise of our independent agents to each bank's best customers. We were only looking for a limited number of referrals so we could focus our service on them and really provide added value to them. It turned out to be the right approach because we were able to show the bank executives that we were there to protect and help their best customers and enhance the relationship the banks had with them. We were not at all a threat to their relationship with their customers."

The result is that Bankers Insurance boasts a referral to close ratio of around 36%--mainly commercial lines and benefits business. The agency has property/casualty premium volume of around $50 million and employs 100 people. It also generates $1.5 million in revenue from life and benefits business. A number of past presidents of the Big "I" of Virginia are involved with the agency.

Vernell concludes by pointing out that Bankers Insurance brings a lot to the table that benefits both customers and agents. "We bring a lot of resources into the equation. We should have a common database for all our branches that will be connected with high-speed lines. We've also upgraded their phone systems where that was necessary. But probably most important of all is the fact that, going forward, they will always be able to afford the best hardware and software and have access to the best markets."

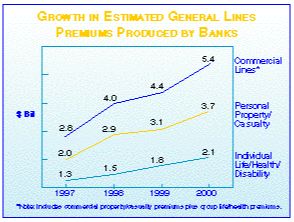

Banks have made serious in-roads into the insurance business. The ABIA and Reagan Consulting study found that bank-produced insurance premiums totaled approximately $44.9 billion in 2000. While the majority of this was from annuities and credit insurance, their general lines (property/casualty and life/health) premium volume totaled around $11.2 billion. This represents total growth of 22.3% overall and 20.4% in general lines. The fastest growing sector was commercial property/casualty insurance, which rose 23% to $5.4 billion in 2000, from $4.4 billion in 1999. Clearly, they are a force to be reckoned with ... or perhaps, partnered with.

Copies of this study can be purchased by calling ABIA at (800) BANKERS. *