GROWTH STRATEGY REVIEW

Agency faces up to problems with cash flow and operations, takes action to land on its feet

By G. Edward Kalbaugh

This case study illustrates how one agency lost its direction, found itself in serious trouble, almost went bankrupt, was rebuilt, and ultimately returned to growth and profitability.

The study identifies various initiatives undertaken over three years to achieve the turnaround, increase the on-going reward to owners and key staff, and improve the agency's value in terms of a potential sale.

The name of the agency and certain financial data and operational information have been changed to protect confidentiality requirements. However, these changes were made in a manner that preserves the integrity of the case study and the valuations achieved.

The ABC Agency was in trouble. Within 18 months, six major clients worth $2.5 million in commercial premium had non-renewed, personal lines commission revenues had declined by 20%, two insurance carriers had terminated their contracts, and customers were complaining they had paid premiums but never received policies.

The owners, involved in other business ventures for several years, had essentially turned the agency over to family members severely lacking in business experience and management skills. Additionally, several staff in key positions lacked insurance expertise and, worse, tried to cover up their deficiencies by hiding or destroying records. Morale was extremely low.

Crisis management

The owners finally received a wakeup call when their largest commercial customer threatened to change agencies. The ensuing discussion led the owners to request help.

It was agreed that the immediate requirements were to address the most critical problems while ensuring that no further damage ensued. Accordingly, a crisis management plan was developed and set in motion. Outlined below are components of the plan, some of which were initiated concurrently.

Business and operational plan--The first step was to develop a business and operational plan defining how the agency would overcome its problems, move forward and grow profitably. The plan, which included detailed premium and financial projections, was the starting point for communicating and negotiating with insurance companies.

Insurance company support--The second step consisted of meetings with senior executives from the agency's primary insurance companies to describe the problems and achieve solutions.

The agency's premium volume was $3.2 million in personal lines and $4.6 million in commercial lines, with 70% distributed among six insurance companies. Each company agreed to provide information for all policyholders, as well as all related accounting information.

Policyholder records reconciliation--The agency could no longer rely on its computer records because much information had not been entered or was missing. Therefore, a secure area was set up as a "war room" where a team of key staff reconciled paper records with computer files and information from insurance companies.

With reconciliation completed, the agency was assured that the insurance requirements of all customers were addressed, and that computer records were accurate and complete. Also, the agency now had a baseline from which to measure progress.

Customer relations--Certain members of the team were assigned to resolve open critical customer issues concerning policy issuance, endorsements and claims. As individual policyholder information was reconciled, these team members called the customer to confirm the account status. These calls were followed with a letter from the agency owners. At the end of the process, all customers had received a call and a letter.

Personnel--The records reconciliation and reconstruction effort revealed that three employees had hidden and/or destroyed records. Accordingly those employees were terminated within one week of the project. The agency now employed 16 people, not counting the owners.

Path to recovery

The business and operational plan provided budgets and a roadmap that enabled the agency to begin a turnaround. Components of the plan are described below.

Staff assessment--Interviews and testing determined the knowledge and skills of all agency personnel, including the owners. These profiles resulted in five additional terminations, four reassignments, salary adjustments, establishment of a training and education program, and initiation of hiring to fill key positions, including outside producers.

Reorganization--The agency immediately hired two new personal lines customer service agents (CSAs), one new commercial lines CSA, one producer, and reorganized to establish:

* A personal lines team (6) and a commercial lines team (3) consisting of licensed, certified CSAs, with each member rotating every three months as team leader

* A sales center consisting of one personal lines and one commercial lines producer, led by a senior CSA, assisted by a CSA in training and a receptionist

* An operations team consisting of one member from each of the other teams, led by an accountant

* a management/audit committee consisting of the owners and team leaders

Internal quality control and processing efficiency--A process was established that recorded and tracked all inbound paperwork, customer service calls and sales leads, from inception through completion of activity and recording of results. This closed-loop system included priority setting, work assignment and workload balancing.

The computer system was modified to export data into management decision reports relating to performance and quality control based on any criteria desired. This capability was one of the most important factors enabling management to measure and influence results.

Teams--Staff members, including owners, were trained in the objectives and mechanics of establishing and maintaining effective teams. Team members operated under individual position descriptions and agency policies and procedures, and were accountable for team goals and objectives. The team itself was accountable to the agency business and operations plan goals and objectives.

Agency branding--It was important to change the agency's image and reposition it to compete more aggressively in the commercial marketplace. The objectives were to increase inbound lead flow in personal lines and small commercial accounts while targeting larger accounts in selective industry segments for outbound sales.

To accomplish these objectives, the agency was positioned to the public as three divisions, with advertising and promotion campaigns for each division--Personal Services, Small Business Owners, and Corporate Accounts. These campaigns were managed through the sales center.

Sales center--The sales center was established to perform campaign fulfillment, qualify all leads, develop surveys and proposals, schedule producer appointments, perform data entry and new account setup, monitor all activity and provide management reports.

In support of marketing and sales, new advertising, stationery, brochures and other promotional materials such as newsletters were developed. Much of the promotional material was used in support of targeted sales campaigns, most of which spanned from six to 15 months.

The Personal Services division primarily targeted areas with high-value homes. The Small Business and Corporate Accounts divisions targeted market sectors that fit insurance company appetites. The campaigns were integrated with a disciplined sales process to ensure maximum effectiveness of producers and sales center support staff.

Sales center sales support required purchase of a new telephone system with call management software. The system enabled all calls to be answered by a person, with routing, voice mail, logging and usage analysis, which aided performance measurement.

Results

Insurance company appointments--As part of its business plan and increased focus on sales, the agency initiated a campaign to expand products and markets. The marketplace was analyzed and plans were designed that targeted high-premium, high-quality personal and commercial accounts. Detailed proposals were presented to insurance companies. The proposals included the agency's business and operational plans based on these tentative targets. The plans were finalized based on targets that fit insurance company appetites.

This process included discussions with 30 insurance companies over a period of three months. As a result, the agency obtained full appointments from two insurance companies. In addition, one insurance company that was reducing personal lines commissions nationwide agreed to a three-year moratorium on reducing the agency's commissions. That agreement preserved $230,000 in commissions over the three-year period.

Book profile analysis--As part of seeking company appointments, the agency's personal and commercial books were analyzed to eliminate unprofitable accounts and to develop cross-selling opportunities. Unprofitable accounts were non-renewed. Lower-value accounts were transferred to new producers. Cross-sell opportunities were provided to the sales center. Retention improved from 78% to 92%.

New outside producers--Three producers were hired. One included $0.8 million in personal and BOP premium. One included $1.2 million in high-value personal and mid-market commercial premium. The third producer had worked for a direct writer and had no book.

Producer contracts were established to address performance requirements:

* Incentives for meeting agency goals

* No renewal commission on accounts below a certain gross commission level

* Incremental vesting in new business

* Requirement that each year the agency buy 10% of the book comprised of the smallest accounts

Acquisitions--The agency acquired a $110,000 commission personal lines book at a cost of 1.2 times retained commissions over three years. Account retention was 85% over that time. However, commissions through cross-selling and rate increases brought the total value to $124,000. Existing staff serviced all accounts from that acquisition and the books of the

new producers.

Summary

To their credit, the owners of this agency made a long-term commitment to achieving a turnaround. That commitment included a significant financial investment as well as on-going support to the agency's reorganization and implementation of the various programs.

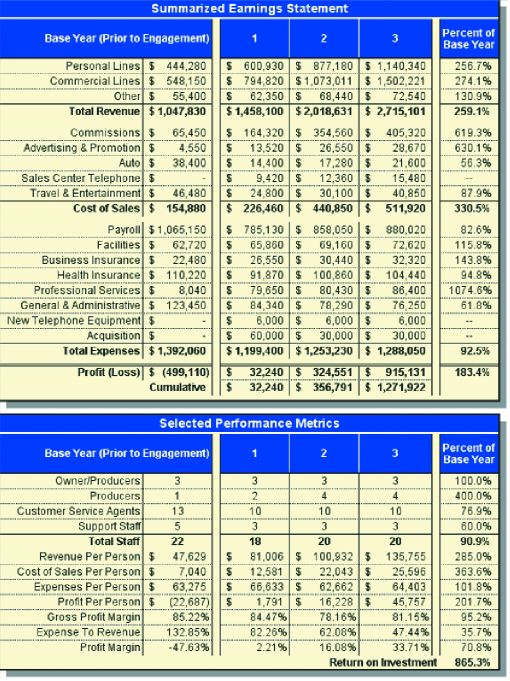

As the financial data indicate, the agency went from a $500,000 deficit to a cumulative profit of close to

$1.3 million over three years.

Primary factors contributing to success of this turnaround included establishing direction and goals through the business model, partnering with the insurance carriers, providing required resources, and then enabling talented people to perform and achieve to higher levels.

Not every agency is in a position to match these results. However, the important points to take from this case study, are that improvement is always possible, that success means long-term commitment, and that agency owners must make the critical decisions that achieve results. *

The author

G. Edward Kalbaugh is a partner at Allegent Growth Strategies, a full-service consulting firm specializing in services to the insurance industry. Allegent is based in Woodbury, New York. Phone: (516) 364-7034, fax: (516) 364-7036, e-mail: info@allegentgsi.com, Web site: www.allegentgsi.com