Source: Tillinghast-Towers Perrin "2001 Directors and Officers Liability Survey"

Source: Tillinghast-Towers Perrin "2001 Directors and Officers Liability Survey"

Accounting scandals add to woes of an already troubled market

By Phil Zinkewicz

Two insurers have filed separate actions saying that they relied on information that contained "material misrepresentation" when issuing D&O policies to Enron. Nine other insurers were ready to jump onto the bandwagon.

First there was the Enron debacle, then Global Crossing, followed by WorldCom, the nation's second largest long-distance carrier, and who knows what company may be next. WorldCom admitted back in June that it had overstated its cash flow by more than $3.8 billion during the last five quarters in what could be one of the largest cases of false corporate bookkeeping yet. Instead of the profit of $1.4 billion the company reported in 2001, and the $130 million in this year's first quarter, WorldCom said that it really lost money during those periods. Basically, WorldCom has been accused of hiding its expenses and inflating its cash flow instead of reporting its losses.

Source: Tillinghast-Towers Perrin "2001 Directors and Officers Liability Survey"

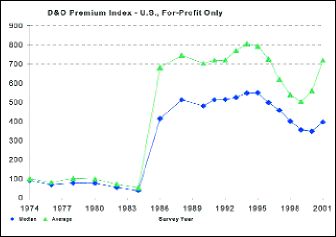

The survey notes that this chart shows that "D&O insurance purchasers in 2001 faced the largest premium increases since the hard D&O markets of the mid-1980s. Premium increases for generally equivalent coverage averaged nearly 29%...."

As in the case of Enron and Arthur Andersen--and Andersen was also the independent auditor of WorldCom--it is entirely possible that the WorldCom situation will result in a spate of lawsuits and many of them could be directed at directors and officers of WorldCom. Insurance companies are already reeling from D&O lawsuits coming from Enron. After the Enron scandal hit the papers, two insurance companies--Royal Insurance Company of America and the St. Paul Mercury Insurance Co., subsidiaries of Royal Sun Alliance and The St. Paul Cos., respectively--filed separate actions in United States Bankruptcy Court of Manhattan, saying that they relied on information that contained "material misrepresentation" when issuing D&O policies to Enron. Nine other insurers, at press time, were ready to jump onto the bandwagon to get out from under the potential D&O liability lawsuits that are expected. If the WorldCom situation follows the same scenario, it could play havoc for the D&O insurance marketplace, at least for publicly traded companies.

It is significant that these troubles follow on the heels of an already troubled D&O market as recently reported on by Tillinghast-Towers Perrin in its 2001 Directors and Officers Liability survey. The survey showed "alarming increases in the costs of litigation against directors and officers, particularly shareholder litigation, as well as widespread concerns about high-profile bankruptcies and the quality of corporate accounting and financial reporting." These things, said the survey, are among the principal reasons for a dramatic increase (29%) in D&O liability insurance premiums. The survey, which included 2,130 participants, is the 24th in a series of studies on D&O liability claims and insurance purchasing patterns.

Although the survey showed that D&O claim frequency remained stable in 2001, severity generally increased, with significant increases for certain types of claims. Among closed claims overall--excluding those closed with no payment--U.S. participants paid an average of $5.65 million to claimants, up more than 75% from the 2000 survey.

The average indemnity paid to shareholder claimants was at an all-time high of $17.18 million, compared to $9.62 million a year earlier.

Source: Tillinghast-Towers Perrin "2001 Directors and Officers Liability Survey"

Source: Tillinghast-Towers Perrin "2001 Directors and Officers Liability Survey"

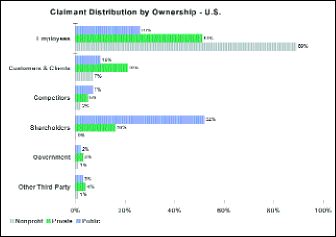

The survey says this chart "illustrates the differences in claimant distribution between the publicly traded, privately owned and nonprofit groups of U.S survey respondents. The most significant increase in the incidence of claims made against directors and officers and their organizations in recent years has been due to employment practices liability."

Issues related to financial disclosure continued to be the most common among shareholder claimants, representing 38.8% of shareholder claims and 9.2% of D&O claims overall. Tillinghast said that disclosures of publicly traded companies are an area of increased concern among D&O insurers due to the significantly higher cost of claims related to such disclosures, including those associated with stock offerings (e.g., IPOs).

The sharp rise of 29% in D&O premiums reported in the 2001 survey, higher than the 11% average increase reported in the 2000 survey, was the most dramatic increase since the hard market of the mid-1980s, according to Tillinghast. However, the survey noted, these increases also represent a reversal of five years of significant premium decreases, which, when combined with the growing costs of litigation, turned insurer profits into losses. The survey also said that, while the total amount of D&O coverage offered by insurers in 2001 was down only slightly from the record levels reached in 2000, many D&O insurers have become increasingly restrictive as to which potential insureds qualify for their full coverage capacity.

"Current conditions do not signal that there is a crisis in the market," said Mark Larsen, a Tillinghast consultant and the survey director. "However, claim severity trends are likely to continue, given the large number of D&O litigation cases outstanding. Companies should diligently evaluate the adequacy of the amount of D&O insurance they purchase and take a longer-term approach in their negotiations to seek the best value. Business class, merger and acquisition activity and financial strength remain key elements of the premiums being quoted," he said.

Another finding of the survey is that the average amount of coverage purchased in 2001 was $20.1 million. Policy limits also increased for the seventh straight year, according to the survey, with U.S. participants obtaining greater limits and less than 5% lowering limits. "Companies see D&O coverage as a necessity in spite of increasingly stringent underwriting by insurers, which requires many companies to build their D&O insurance programs by purchasing smaller layers of insurance than they might wish or by employing quota share arrangements," said Jim Swanke, leader of Tillinghast's Strategic Risk Financing practice.

The survey concluded: "D&O claims were more than twice as likely against companies with a history of merger and acquisition activity, and publicly traded companies were more than twice as likely to experience claims than their private counterparts."

Jack Goodwin, D&O product leader for Royal & Sun Alliance's Professional Financial Risk Division, said that, when looking at the D&O market, one must segment the industry. "There's not-for-profit and private D&O exposures, and then there are the publicly traded risks. The market is hardening in D&O overall; there's no doubt about it. On the not-for-profit and private company D&O side, we're seeing rate increases of 20%, 30% and 40%. There have been some increases in retention, but then retention levels were low for a long time, so it's just playing catch-up and now reflects the growing frequency of EPL type activity. With the publicly traded companies, rate and retention increases are more severe. I've seen rate increases as high as 1,000%," he said.

Goodwin said that the D&O market has built up an inventory of potential losses and that the market has to reflect that. He also said that, on the publicly traded side, it is becoming more difficult to write D&O risks. "When an independent auditing firm signs off on a risk and then says its original analysis was incorrect, that's difficult to underwrite," he said. Goodwin added that, in the future, it might not be unreasonable for insurers to include a "restatement" exclusion in their D&O coverage. "It's not rampant in the marketplace yet, but I've seen it used. Basically, insurers want to see companies take on part of the exposure themselves via higher retentions, and/or coinsurance, rather than passing it all on to the insurer. The time is now for buyers of D&O liability to be financially motivated with their D&O claim." *