Marketing

Survey probes factors influencing agents' choice of carriers

Agents and CSRs give views on claims handling, new business support and more; technology can be crucial differentiator

By Dave Willis

|

|

Life is full of choices. Perhaps nowhere is this truer than in today’s independent agency. Producers regularly decide which product best fits a particular client’s need. CSRs choose which system to access for the quickest or most accurate quote. And, on a more strategic level, principals select carriers they think best match their overall agency focus.

In a recent producer survey, research and consulting firm Celent Communications probed agency professionals who represent AIG/Lexington and Farmers Alliance—the two carriers that invited producers to participate—about what makes them want to do business with certain carriers and not with others. A total of 450 respondents —half of them producers, one-third general agents or agency principals, and one-sixth CSRs—took part in the survey, Independent Producer Survey: Technology, Services, and Other Drivers of Carrier Choice, 2004 Property/Casualty Edition.

From the survey findings, carriers and agencies alike can build up their own organizations, educate staff, and develop better and more profitable relationships with their partners, no matter how many or few there might be.

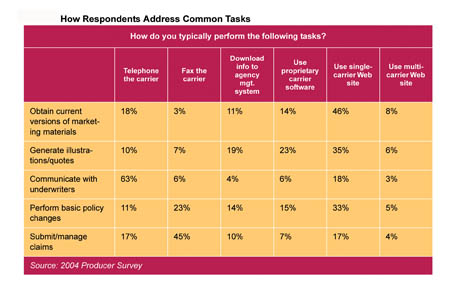

The independent agency system thrives on its ability to tap numerous carriers to provide coverage options. But the number of appointments and the concentration of business among carriers often are two different stories. According to the survey, 70% of agencies and brokerages concentrate the lion’s share of their business with between two and four carriers. Predictably, the diversification is not as marked in personal lines and small commercial, but is greater for middle commercial and workers comp business.

Why one versus another?

What earns a carrier a preferred spot in an agency? To get a clearer picture of the service and technology factors that drive carrier choice, Celent put a little different twist on this year’s survey. Previously, products and pricing were choices. But the firm says these are “the price of admission” and being competitive on them is a core requirement for being considered for a piece of business. So the latest survey focused instead on other factors.

|

|

|

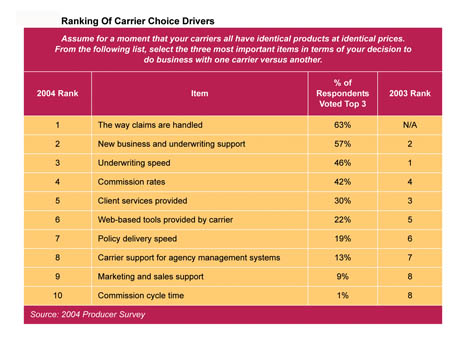

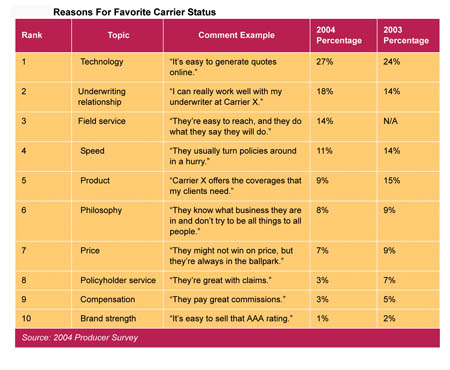

What it found was that claims handling and new business and underwriting support are most important—each chosen as a top item by roughly 60%—when deciding where to place business. (See table, top right.) Underwriting speed ranks third, with just under half of respondents calling it a most significant factor.

Celent explains the prominence of claims service in the standings, saying producers are “keenly aware of the value of satisfied customers” and recognize that their own long-term success “hinges on selling for carriers that meet customer expectations.” To the degree carriers respond to this finding with strong emphasis on claims and claims service, agents and brokers will return the favor with increased business and continued loyalty.

While technology options in and of themselves earn lower rankings on the list, automation can play a central role. For example, new business support and underwriting speed aren’t hard-core tech items; but they are driven by effective technology deployment, and they’re viewed as essential because they fuel a producer’s ability to sell. Celent notes: “Producers expect their partners to make their jobs easier while getting products in the hands of customers more quickly.” Technology “may be a crucial differentiator” to the extent it can affect claims handling, new business support and underwriting speed.

Commission rates rank fourth. Celent believes this indicates that, while producers don’t sell on commission rates alone, they do get producers’ attention. Their prominence on the list also indicates a willingness to provide unbiased opinions—even politically incorrect responses—in an environment marked by increased scrutiny.

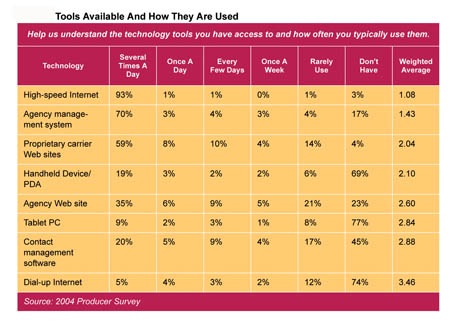

Other trailing factors include client services provided, chosen by 30% of respondents; policy delivery speed, 19%; and marketing/sales support and commission cycle time, each of which earned single-digit responses. Web-based tools provided by carriers was identified as a driver by 22% of respondents, and carrier support for agency management systems was named by 13%.

It depends on whom you ask

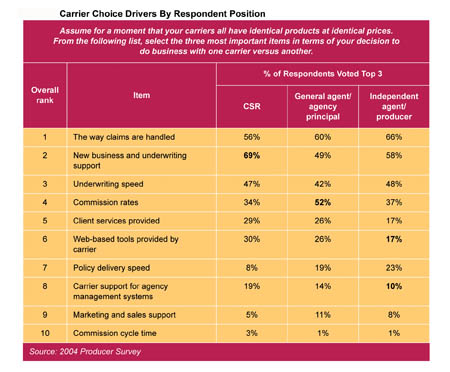

For a closer look at what drives choice, Celent sliced and diced the responses several ways, including by who provided the answers—producers, principals or CSRs. (See table middle of page at right.) Subtle differences surfaced, but none are particularly surprising, Celent says.

For instance, agents or producers—those with face-to-face customer contact—most often list claim service as a top item. CSRs, on the other hand, are most likely—at about 70%—to rank new business and underwriting support as tops. Fewer than 60% of producers and 50% of principals concur.

There was across-the-board agreement on the role of underwriting speed, with about 45% citing it. Differences appear in the commission rates ranking, though. More than half of GAs and principals place this on their list of top-three carrier choice drivers, compared to roughly one third of producers and CSRs who do.

Principals and producers are more than twice as likely as CSRs to list policy delivery speed as most important, and principals are more inclined than their co-workers to mention marketing and sales support.

On the technology questions, CSRs are nearly twice as likely as producers or agents to view Web-based tools provided by carriers or carrier support for agency management systems as key factors in choosing one carrier over another. Principals take the middle ground on these, but cite, by almost a two-to-one margin, Web-based tools over carrier support for management systems.

Now you know; so what?

As any veteran businessperson knows, the value of a survey isn’t so much in its data as in actions that emanate from it. That’s true for carriers and agency staff alike. Those inclined to discount the results may prefer the wisdom of the late British politician Benjamin Disraeli, who said, “There are three kinds of lies: lies, damned lies, and statistics.” Those wishing to improve operations, however, can find insight and direction in the results.

|

|

Carriers can work to understand what their particular producers value. They should ask producers what it is about their claims handling—or another company’s—that’s good or bad. What new business and underwriting support attributes drive producer satisfaction? How speedy does underwriting have to be, and does the answer depend on who’s being asked or what line of business is involved?

According to Celent, as carriers bring on new initiatives, they should target various user groups separately and communicate specific benefits they provide each group. Clearly, by understanding what motivates a CSR vs. a producer or principal, carriers can design services and support more effectively and communicate better.

By the same token, understanding differences and addressing them, perhaps through focused staff meetings or some other communication mechanism, can help agencies strengthen their own operations. Principals should pay attention to what producers and CSRs think, and how that differs from—or tracks with—their own ideas. For instance, are 70% of CSRs right in saying that new business and underwriting support are among the most important factors? If so, why do just under half of principals come up with the same answer? Do producers and CSRs lack understanding of the role commission rates play? Or do principals overstate it? What can CSRs learn from producers about the value of claims handling or policy delivery speed?

All of these questions highlight the need for better communication and understanding within an agency and a focused, strategic approach to carrier selection. By devoting time—by being willing to teach and learn—principals can drive increased operational efficiency. And they can help their agency live out an admittedly taken-out-of-context quote from 17th century English poet Francis Quarles: “Be very circumspect in the choice of thy company.” *

For more information:

Celent Communications

Web site: www.celent.com

Phone: (617) 262-3120

The author

Dave Willis is a regular contributor to Rough Notes magazine on insurance technology, sales, marketing and agency management issues.