|

|

|

|

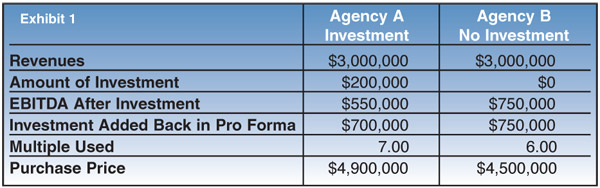

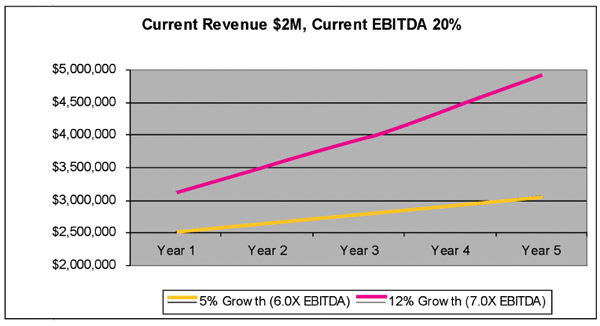

Building Equity Value So, you've decided to sell your agency Examine income stream, balance sheet and other determiners of value By Chris Darst As agency owners contemplate their desired exit strategies, two fundamental options exist for divesting stock: perpetuate internally to existing producers and/or employees, or sell the agency to an outside third-party buyer. While many agency owners would commendably prefer to perpetuate internally, it can be a difficult process that requires a long-term commitment from both buyers and sellers of stock. Without extensive planning, personnel willing and able to finance a personal buyout, a consistent transition of roles and responsibilities, and broad ownership, internal perpetuation becomes increasingly elusive for many owners. For those who cannot financially or logistically make internal perpetuation work, an external sale may be inevitable. For others, an external sale may, in fact, be the exit strategy of choice. In either situation, owners need to be cognizant of some basic considerations when divesting externally. Some things to consider Buyers take into consideration many factors when placing a value on an insurance agency. To an agency owner, many of these are obvious, but there are some that you may not have considered. Understanding Agency Values— There are two components of agency value. The first is the book of business value, which is a value of the earnings stream; and for an insurance agency, this is typically the most significant piece of the value equation. In the insurance industry, book of business value is commonly expressed as a multiple of revenue; however, actual value is calculated as a multiple of sustainable earnings or pro forma EBITDA (Earnings Before Interest, Taxes, Depreciation, Amortization). In the simplest terms, buyers will create a pro forma income statement to determine the amount of sustainable earnings that can be generated from an agency’s current operations, and this amount is multiplied by a risk factor to determine price. In today’s marketplace, the EBITDA multiple usually falls between 5.0 and 8.0 times, but we have worked on deals with multiples in excess of 8.0 times EBITDA (usually due to sellers exceeding expectations during the earn-out period). The second component of value is the balance sheet. The value of the balance sheet equals total equity less intangible assets. The value of the balance sheet is typically added to/subtracted from the book of business value at close, the consideration of which is contingent upon the deal structure and parties involved. Selling Agency Prior to Retirement—Buyers often request that key employees/owners continue working for a number of years subsequent to the close of the transaction to help transition key relationships, solidify major accounts, and transfer management responsibilities. Agencies that lock in key employees for a number of years after close usually command a higher price than those agencies where the owners and key employees are ready for retirement. Perpetuation Planning—Even though you plan to sell your agency, you should still have a perpetuation plan in place. Perpetuation is not simply a transaction of buying and selling stock. It is an overall philosophy for continued growth, predictable profits, strong leadership and personnel, and increasing agency values. An agency that has a perpetuation plan in place will typically be more attractive to buyers and generate a higher price than an agency with no plan. Why? Because the agency does not necessarily have to sell, but rather controls its own future. Accentuate a Sales Culture—Buyers are more attracted to agencies that practice sales management techniques to enhance producers’ W2s and promote a total agency sales culture. Some of these sales management tools are listed below. • New business minimum: 20% of prior year book • Annually trade down: bottom 20% of accounts • Annually recalculate average account size—set minimum • Minimum book size • Defined roles and responsibilities • Circulate producer performance relative to plan • Staff bonus tied to producers attaining goals • Implementation of defined value-added service plans • Formalized referral request process Continue to Invest in the Future—Sellers often refrain from hiring new producers or investing in new technology prior to selling their agency because they believe that these kinds of investments will negatively affect the agency’s earnings and therefore the purchase price. However, our experience is that these kinds of investments exponentially enhance the value of an agency. Exhibit 1 illustrates this point. Although it is a negotiable item, most buyers will give a seller credit on the pro forma for investing in producers and technology. In other words, if an agency spends $200,000 investing in new producers, a buyer will typically add a significant portion of the investment back in the pro forma for the purposes of calculating pro forma EBITDA. Furthermore, since the agency has upgraded its technology and has invested in young producers, the risk factor (EBITDA multiple) used to price the agency is justifiably higher than it would be otherwise. The exhibit assumes that 75% of the investment is added back to the pro forma. Balance Sheet Management—You can tell a lot about an agency by how well its balance sheet is managed. A buyer will meticulously analyze a seller’s balance sheet and come to speculative inferences about the agency based on this analysis. A buyer will relate a weak balance sheet to a management team that is feeble and incompetent. Trust issues, poor collection practices, and debt problems will all lead to a lower purchase price. Off-Balance Sheet Liabilities—Many owners overlook obligations or liabilities that aren’t reflected on the balance sheet. These obligations cannot be forgotten when determining the value of an agency. The most common off-balance sheet liability we see is deferred compensation agreements with producers, and this needs to be accounted for when calculating agency value. Ownership of Books of Business—You can’t sell something that you don’t own. The vested portion of producer books or outside producers who own their books of business are excluded when determining agency values. Even though they are not upheld in some states, we recommend that owners require producers to sign employment agreements with non-compete/non-solicitation language specifically identifying who owns what business, prior to negotiating with buyers. Correlation Between Growth and Value—Most agency owners understand that growth is a factor when assessing the value of an insurance agency. However, few owners understand the full impact that growth has on agency values. Not only will buyers assess risk based on historical growth levels, but the amount of proceeds received from the sale is usually predicated on future growth levels achieved during the earn-out period. Strong historical growth helps to justify a higher than average EBITDA multiple when pricing the agency. Exhibit 2 illustrates this growth to value concept. Exhibit 2 assumes that an agency with 5% historical (and projected) growth may command a multiple of 6.0 times EBITDA and an agency with 12% historical (and projected) growth may justify a multiple of 7.0 times EBITDA. The reason for the higher multiple resides in the increased potential to drive revenue, earnings and value. Growth is extremely important to the value of an agency, and partnering with the right buyer could complement growth initiatives. However, integration can be a slow and difficult process, and it could take a few years before the agency is running on all cylinders. Our experience is that the agencies that perform well subsequent to close are those agencies that performed well prior to being purchased. These agencies possess strong organic growth initiatives and have created a total sales culture within their organization. Whatever the motivation for selling an agency, there are ways to make your agency more desirable, and thus valuable, to potential buyers. The key resides in understanding internal agency value drivers and the external buyer marketplace. The next article will document and describe the various external buyer segments. * The author |

|

|||||||||||||

| ||||||||||||||