|

|

|

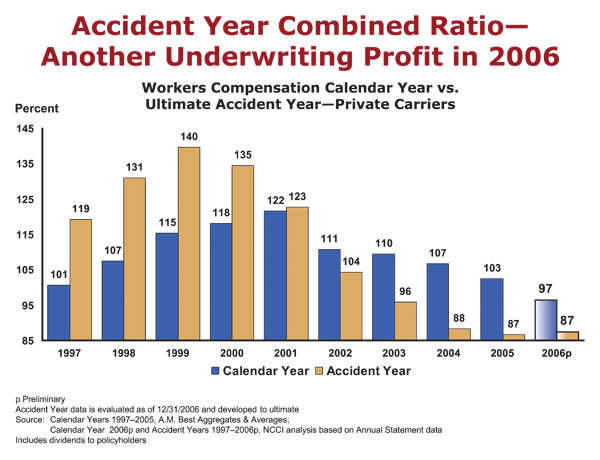

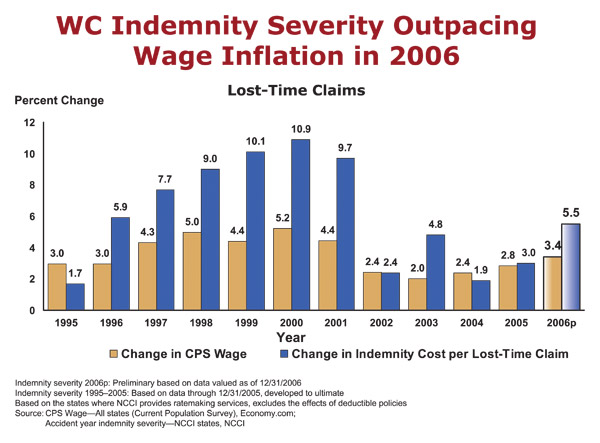

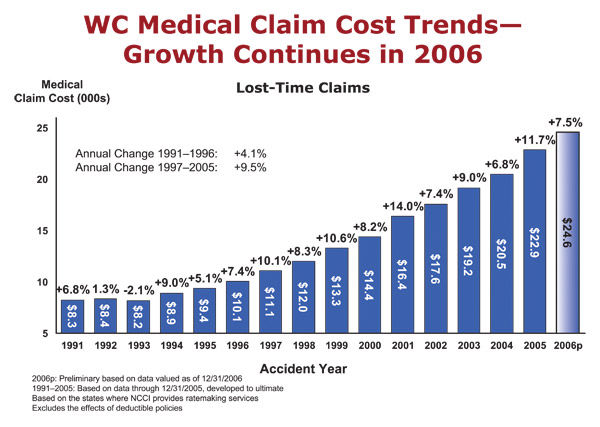

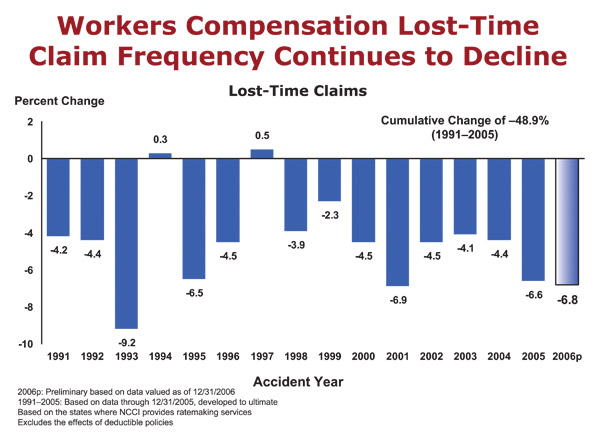

Everything's comin' up roses Comp underwriters are happy but cautious By Dennis H. Pillsbury It’s hard to imagine a gathering of workers comp executives where everyone is smiling, even before the cocktail reception. But that was exactly what happened as the NCCI hosted its Annual Issues Symposium last May in Orlando, Florida. Of course, there were unusual circumstances. There hasn’t been this much good news for comp carriers in quite a while. And even the weather added to the jovial mood. The event was threatened by smoke that was billowing over much of Florida, but favorable winds cleared the skies so there was hardly a whiff of smoke at either the opening or closing reception, both of which were held outdoors. And the brief shower that marred the closing reception only resulted in the bars staying open an extra hour. The attendees heard NCCI Chief Actuary Dennis C. Mealy, FCAS, MAAA, report that in 2006 the workers comp line enjoyed “the best combined ratio in over 30 years”—96.5%. Considering that a mere five years earlier, the workers comp combined ratio stood at an abysmal 122% in 2001, this is certainly reason for the cautious ebullience that permeated much of the meeting. In his State of the Line address, Mealy continued with the good news by pointing out: “Our estimates of the reserve position of the private carriers also continued to improve. The deficiency, which peaked at $21 billion at year-end 2001, has declined to $4 billion at year-end 2006. After consideration of the allowable discounting of the indemnity reserves of lifetime pension cases, the industry’s reserve position is one of essential adequacy, a tremendous improvement over the last five years.” He went on to caution, however, that much of the improvement came from California where reforms have had a major impact on results. If California’s numbers were excluded from the results, the combined ratio would be over 105% and “the accident year combined ratio would rise from 87% to 95%. This puts the results for the rest of the country in the context of good but not great,” Mealy pointed out. And there was yet more good news. Lost-time claim frequency continued a decades-long decline. However, Mealy noted, “On the severity side, we saw indemnity costs creeping up a bit after moderating over the last few years.” Mealy summed things up by noting that “NCCI’s short-term view of the line remains optimistic. However, the long-term view remains cautionary due to the long-term challenges that continue to face the business.” Now for the not-so-good news It hardly comes as a surprise to any observer of the workers comp industry that medical costs have been and continue to be the number one concern. As Mealy pointed out, “Medical cost increases continue largely unabated and put upward pressure on costs.” In 1986, medical losses accounted for 45% of total losses. In 1996, medical costs accounted for 52% of total losses and in 2006, they accounted for 59%. Other concerns enunciated by Mealy included: • “Low investment yields, particularly for longer term investments, mean that combined ratios need to be at or near historic lows for insurers to earn an adequate return on capital.” He noted that the combined ratio for 2006, despite being the best in more than 30 years, did not produce anywhere near record rates of return. The post-tax return on surplus was “only modestly above the average for the last 20 years.” • Prosperity produces legislative interest that may not be favorable to comp insurers. “We have observed increased activity on the legislative front in 2007 versus 2006.…In some states, there has been renewed interest in revisiting issues that had been dealt with in past reforms.” He warned that, given the positive results, “Some parties may feel that now is a good time to review benefit levels, administrative guidelines, and cost controls, to the possible detriment of efficiently running a well-balanced workers compensation system.” • “The Terrorism Risk Insurance Extension Act (TRIEA) is expiring at the end of 2007.” Mealy went on to point out that NCCI modeling of the terrorism exposure makes it clear that “TRIEA is critical to the survival of the insurance industry in the event of a devastating incident.” • “The current underwriting cycle is likely at its cyclical peak.” Yesterday’s news One of the interesting topics in recent years has been the impact of the baby boomers in such areas as Social Security, Medicare, health care, and workers comp. Well, at least in workers comp, the impact of the baby boomers is “yesterday’s news,” according to Mealy. “Baby boomers did lower the average age of the workforce about 3.5 years from the time they began to enter the workforce in the early 1960s until they were largely integrated into the labor markets in the mid-1980s. “Subsequent to the mid-1980s, the average age of the workforce rose to pre-baby boomer levels as the baby boomers aged,” Mealy continued. “However, demographic projections from the Bureau of Labor Statistics indicate that the average age of the workforce will stabilize at or near current levels for the next 40 years.” It will certainly be interesting to see whether we still have a plethora of smiling workers comp executives at next year’s Annual Issues Symposium. There appears to be some cause for cautious optimism, but the uncertainty of passage of TRIEA and the industry’s own propensity to shoot itself in the foot whenever it starts to see profitability will certainly play well with those atrabilious prognosticators who have been relatively quiet over the last few years. However, there continue to be many, including Mealy, who believe that “this cycle may be less severe than the last one.” Could it be that the industry has finally learned? Only time will tell. But we all certainly would welcome pricing stability. As one risk manager told me: “We need rate stability. Modest increases can be understood by business people, but not the huge changes that accompany cyclical turns. I have just as much trouble explaining huge decreases in premium as I do explaining huge increases. Neither one makes sense to my boss. I know exactly what I will hear when I come in with either one of those. ‘How do they run a business like that? We’d be out of business if we priced our product like that.’ And, of course, when I have to present a huge increase, I’m always concerned that I might hear something worse. “That’s one of the reasons we’re looking at the alternative market,” he concluded. The loss of significant market share to the alternative market might be just the impetus the industry needed to put its house in order. The risk management community no longer has to sit back and tolerate cyclical swings. Nor will it. * |

|

||||||||||

|

|||||||||||