|

|

|

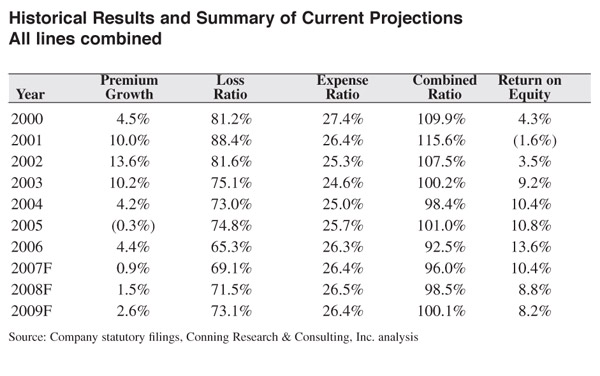

Special Section Sponsored by Target Markets Program Administrators Association Forecast Looks Good for Program Administrators New Conning study makes line-by-line projections By Phil Zinkewicz The current soft market, for as long as it lasts, promises to be good for the program administration arena, at least in terms of the availability of carrier markets. Carriers are looking favorably upon program administrators, anticipating new diversification that might bring in new premium dollars at a time when competition in the standard market is increasing and new premium dollars may soon be dwindling. Moreover, according to Conning Research and Consulting, the soft market is likely to persist into 2009, emphasizing the program administrator’s importance in the program business scenario. For program administrators, the Conning report might be particularly helpful as it makes projections about market conditions, line by line, through 2009. Titled “Property-Casualty Insurance Forecast Through 2009,” the report quotes Stephan Christiansen, director of Conning Research, as saying that the 2006 underwriting results were a watershed for the insurance industry. “The combined ratio dropped to 92.5%, based on preliminary data,” he said. “The implied GAAP return on equity was a remarkable 13.6%, with a positive cash flow of over $58 billion. Policyholder surplus grew $63 billion to $506 billion.” However, one key issue, according to Christiansen, is whether the market is on the precipice of a meltdown, with price cuts that undermine premium and rate adequacy. “At this point, we have not observed rampant, reckless behavior and do not forecast a competition-driven market meltdown,” he said. “Rather, we more expect ‘death by a thousand cuts’ with a combination of deteriorating premium rate adequacy, increasing loss severity and limited growth in investment yields.” Regarding competition in the marketplace, Christiansen said that at the end of the second quarter of 2007, price competition was increasing for most major lines of business. “Insurance buyers and agent/broker surveys and other insurance pricing monitors indicate mid-single-digit to low double-digit decreases for commercial insurance.” The Conning report says that, if price decreases continue to accelerate, it will not take much time before discounts erode premium rate adequacy. Christiansen pointed out that it is difficult to forecast when and where insurers will moderate price decreases. Breaking down industry projections line by line, the report says that personal automobile pricing is softening after four consecutive years of underwriting profits. “The combined ratio for this line is forecast to increase going forward with competitive pressure on rates driving the ratio back to 100% by 2009,” according to the report. “The decreasing claim frequency trend appears likely to continue, but the steady increase in severity is forecast to continue as well.” The homeowners line remains healthy, according to the report, with three of the past four years recording sub-100% combined ratios. Results in 2006 benefited from a very low level of insured catastrophe loss activity, combined with rate increases following the hurricanes of 2004 and 2005. The report notes that competition is expected to return to the homeowners insurance market following this run of profitable growth, although the combined ratio should remain at levels below 100%, assuming more typical catastrophe losses. Commercial automobile results began to deteriorate in 2006, according to Christiansen. “We expect competition among insurers to erode premium rate adequacy into 2009,” he said. “An important question is how soon insurers will react to the worsening results. This forecast anticipates that enough insurers will take pricing management actions sometime in 2008 and 2009 to begin slowing the industry deterioration in the combined ratio. However, this is contrary to prior soft market development trends, when underwriting results had to get much worse than breakeven before the market reacted.” Although workers compensation profitability has improved consistently since 2001, Christiansen’s forecast through 2009 suggests that several factors could reverse this trend, including increased price competition and the potential for increasing losses. In the commercial multi-peril arena, Christiansen said that large underwriting profits in 2006 are giving way to substantial price decreases and premium rate erosion in 2007. “Competition continues to increase with emphasis on ‘Main Street’ with general price decreases approaching double digits, except for flattening prices for catastrophe exposures. “Although insurers continue developing coverage enhancements and broadening eligibility … the enhancements do not appear to be substantive enough to have other than a minor effect on premium rate erosion for the industry,” Christiansen reported. The general liability lines continue to show a remarkable recovery in profitability, according to the Conning report. “Cautious of the history of volatility in this long-tailed line, our forecasts through 2009 suggest that a leveling in results, and possible turnaround, may be in the offing,” said Christiansen. As for medical malpractice, the report says that the line has been doing remarkably better than it was a few years ago. Nevertheless, the improvement can be short-lived, based on a sudden rise in price competition and/or losses. “As a result, our projection through 2009 predicts deterioration in results, albeit not a dramatic one,” said the Conning researcher. Medical malpractice earned a positive ROE in 2006 amid stabilizing loss trends, says the report. Statutory data show a 90.6% combined ratio. “The remarkable result is at least partially due to significant releases of past years’ reserves,” Christiansen observed. “Calendar year changes to accident-year incurred losses have been negative since 2002. Our forecast is for the combined ratio to continue relatively steady, though slightly up in 2007. How long the trend lasts depends on the longevity of the tort reform movement, and the strength of price competition in response to the line’s new-found profitability.” Continued Christiansen: “Tort reform continues, with additional bills introduced at the state level in 2006. These include continuing emphasis on caps, limitations on attorney fees, inadmissibility of apologies and expert witness standards—but also increasing emphasis on greater accountability for insurance company reporting and on controls on rate activity. “Loss frequency appears to be dropping, although severity may have increased again after two years of apparent leveling,” he said. “Our projections are based on a slight deterioration in the loss ratio into 2009, as the novelty of tort reform wears off, and considering at least the potential for reversal in some jurisdictions.” Continued exposure growth and a very low level of insured catastrophe losses in 2006 produced record results for the inland marine lines of business, according to the Conning report. New premiums grew 11.9% for the year and losses were down 14.5%, resulting in a combined ratio of 72.8%. Conning projects continued underwriting profitability, with combined ratios less than 90% continuing through 2009, assuming normal catastrophe losses. Finally, on nonproportional reinsurance, the report states that overall, results indicate underwriting profitability for 2007, partly driven by low catastrophe losses. “We forecast results to deteriorate with more normal catastrophe losses, as the market moves into a softer underwriting cycle and premium rates and reinsurance rates are pressured downward, and as inflationary factors continue to increase loss severity.” → |

|

|

||||||

|

||||||||