Personal Lines

The Farmowners Policy: A Personal/Commercial Hybrid

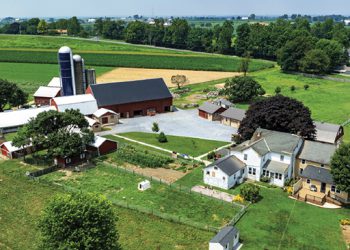

Farm Ag conference sessions go “back to the basics” By Christopher W. Cook Earlier this year, I attended the Big...

Inflation, Personal Auto And Risk Management Choices

Managing private passenger cost increases without boosting exposure to loss Advising insureds about how to reduce their exposures can help...

Coverage Denied for Driver Who Transported Marijuana

Popular “gigs” create cover problems ith a growing gig economy … the lines between business and personal activities have become...

PERSONAL LINES WATER-RELATED CONSIDERATIONS

Are they simpler than commercial lines? rge your clients not to skimp on the water backup limit of insurance, as...

Is Parametric Coverage An Innovative Solution To Rising Deductibles?

Product that addresses challenges of severe weather events gains traction By combining parametric with traditional property insurance, insurance professionals can...