The insurance brokerage sector

looks to balance economic uncertainty

against M&A deal volume and valuations

[We are] seeing buyers increasingly differentiating between

firms with sustainable, producer-led organic growth

and those whose recent performance was primarily market-driven.

By James Graham, CVA

The insurance brokerage merger and acquisition (M&A) market remains active in 2026, but the dynamics underpinning dealmaking have shifted meaningfully over the past 12 to 18 months. After several years of a hard insurance market fueled by strong, rate driven organic growth and record valuation multiples, the industry is now transitioning into a softer pricing environment.

This shift is reshaping buyer expectations, seller behavior and, ultimately, how brokerage firms are valued.

With slowing or declining property and casualty (P&C) rate increases comes more pressure on organic growth, which had been buoyed for years by premium inflation rather than pure new business production. Public brokers reported a noticeable deceleration in organic growth during 2025, with many falling from near double-digit growth rates to the mid-single digits as pricing tailwinds faded.

This softening insurance cycle has impacted the public broker stock values, as investors rotate out of the sector.

Despite public broker valuations falling, there has not been an immediate downstream impact across independent (founder-led) broker valuations. According to MarshBerry’s proprietary database, valuations for both average of all firms and platform firms remained elevated to start 2026. Valuations as a multiple of EBITDA on an upfront base purchase price ending Q1 2026 averaged 11.52x across all firms, with platform firm valuation multiples averaged 14.19x on an up-front base purchase price.

One of the byproducts of slowing organic growth is the even more critical strategic lever that M&A offers. Many acquirers are using acquisitions to offset decelerating internal growth, expand specialty capabilities, and gain scale advantages in a more competitive pricing environment.

However, MarshBerry is seeing buyers increasingly differentiating between firms with sustainable, producer-led organic growth and those whose recent performance was primarily market-driven.

As speculation continues on the potential for a lowering of valuation multiples, the market is still flush with buyers who are well capitalized. Firms that are able to generate sales velocity in the mid-to-high teens are still commanding aggressive valuations as the buyers are continuing to look for ways to enhance their own organic growth metrics.

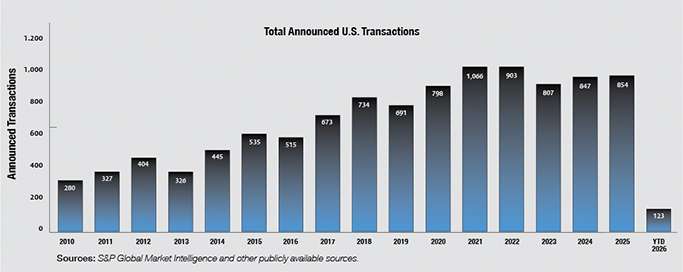

So, despite the softening market and slowing organic growth, M&A transaction volume has proven resilient. M&A activity for insurance brokerages in 2025 finished as the third highest volume year on record, driven largely by private equity-backed platforms and well capitalized strategic buyers flush with dry powder. While deal counts moderated slightly in the first quarter of 2026, demand for quality assets continues to outstrip supply.

In sum, the insurance brokerage M&A market remains fundamentally healthy, but the rules of the game are evolving. A softening insurance market is not derailing deal activity, yet it is reinforcing a return to fundamentals—where true organic growth, operational discipline, and strategic fit matter more than ever in driving valuation and successful transactions.

The author

James Graham joined MarshBerry in 2015 and is a Managing Director on MarshBerry’s Financial Advisory team in its Dana Point, California, office. His expertise includes merger and acquisition advisory, capital raising, business valuation, perpetuation and succession planning, and strategic planning. James provides his clients with customized financial and capital strategies to help them accomplish their goals. He also is a facilitator for MarshBerry’s Connect Network and actively publishes articles relevant to the insurance distribution marketplace.

MarshBerry is a global leader in investment banking and consulting dedicated to helping insurance brokerages, and firms in the wealth management industry and the accounting and tax industry, achieve sustained growth and value for every stage of ownership. With a legacy spanning over 40 years, MarshBerry offers an extensive suite of services, including investment banking (merger & acquisition advisory; capital raising), financial consulting (strategic planning; valuations; perpetuation planning), organic growth consulting (leadership, sales & talent solutions), executive peer exchange, agency network and market intelligence and performance benchmarking.

M&A Market Update

Through March 31, 2026, there were 123 announced M&A transactions in the U.S.—representing a 4.9% decrease over the same period in 2025. Keep in mind, a similar trend occurred in early 2025 due to uncertainty in the broader macroeconomic environment, only to have the year end with the third highest number of M&A transactions on record.

Out of those 123 deals, private capital-backed buyers accounted for 86 (69.9%) of them, while independent brokers were buyers in 15 deals, or 12.2% of the market. There have been only two announced transactions by bank buyers so far this year. Deals involving specialty distributors as targets accounted for 32 transactions, representing 26% of the total market.

Deal activity from the marketplace’s most active acquirers remains strong in 2026. Ten buyers accounted for 52% of all announced transactions, while the top three (BroadStreet Partners, Inszone Insurance, and ALKEME Insurance) account for 26% of the 123 total transactions.

Notable Q1 2026 transactions

January 21: EPIC acquired The Bond Exchange, a California-based surety bond agency, adding specialized underwriting and brokerage expertise to its national surety practice. Founded in 1999, The Bond Exchange brings deep experience supporting complex surety programs across industries such as construction, real estate, mining, renewable energy, technology, and private equity.

The acquisition expands EPIC’s ability to serve large, sophisticated clients while also enhancing efficiency for smaller bond placements through The Bond Exchange’s technology-enabled platform. The transaction supports EPIC’s continued investment in building a scaled, integrated surety offering with broader geographic reach and enhanced technical capabilities. MarshBerry served as an advisor to The Bond Exchange on this transaction.

January 30: Novacore agreed to acquire CP Insurance Associates (CPIA), a Texas-based insurance services agency focused on lender-placed insurance and coverage programs for financial institutions and specialty lenders. Founded in 1977, CPIA serves banks, mortgage servicers, credit unions, and other lending-focused clients with collateral protection, compliance support, and technology-enabled insurance administration.

The acquisition strengthens Novacore’s position within the financial institution and lending ecosystem by adding a long-established platform with specialized expertise. The transaction supports Novacore’s strategy of expanding its portfolio of specialty MGA solutions and scaling lender-focused insurance offerings nationwide. MarshBerry served as an advisor to CP Insurance Associates on this transaction.

Investment banking services in the USA offered through MarshBerry Capital, LLC, Member FINRA and SIPC, and an affiliate of Marsh, Berry & Co., LLC. 28601 Chagrin Blvd., Suite 400, Woodmere, Ohio 44122 (440) 354-3230)

Disclosure: All deal count metrics are inclusive of completed deals with U.S. targets only. Scorecard year-to-date totals may change from month to month should an acquirer notify MarshBerry or the public of a prior acquisition. Statistics are preliminary and may change in future publications. Please feel free to send any announcements to M&A@MarshBerry.com.